In his annual letter to company investors, BlackRock CEO Larry Fink urged politicians and corporate leaders to come together to address the retirement crisis.

Fink, 71, highlighted the economic anxiousness of Millennials and Gen Z when it comes to retirement and stated that they are right to believe that his generation, the Baby Boomers, “have focused on their own financial well-being to the detriment of who comes next.”

“As a society, we focus a tremendous amount of energy on helping people live longer lives,” he wrote. “But not even a fraction of that effort is spent helping people afford those extra years.”

Larry Fink, chairman and chief executive officer of BlackRock Inc. Photographer: Victor J. Blue/Bloomberg via Getty Images

Larry Fink, chairman and chief executive officer of BlackRock Inc. Photographer: Victor J. Blue/Bloomberg via Getty Images

In the letter, he points to a March 2023 report from the Social Security Administration that shows by 2034, the system will not be able to pay people full benefits.

Fink writes that the current message the workforce receives from the government and corporations is, “You’re on your own.”

“Before my generation fully disappears from positions of corporate and political leadership, we have an obligation to change that,” Fink wrote.

The letter also suggests reevaluating the standard retirement age.

“No one should have to work longer than they want to,” Fink wrote. “But I do think it’s a bit crazy that our anchor idea for the right retirement age — 65 years old — originates from the time of the Ottoman Empire.”

Instead of moving back when people receive retirement benefits, Fink suggests having conversations about how to encourage people to work past 65 years old and how to treat that demographic differently, as people with a lot to offer instead of ready for retirement.

Recent data from the Employee Benefit Research Institute (EBRI) shows that the median age for retirees is 62 and the mean is 65 years of age, even though workers are more likely to say that they expect to retire at 70 or older.

Almost half of retirees who left the workforce earlier than they wanted to retire said they did so because of health problems, disabilities, or shifts at their company.

Only 35% of people who retired earlier than planned did so because they were financially ready for retirement.

Related: Can You Afford to Retire? Here’s How Much Americans Spend Daily in Retirement

Fink also stated that BlackRock would announce partnerships and initiatives over the next few months to ask policymakers, investors, retirees, and other interested parties about how the average retirement age should change.

Other solutions Fink proposed were making investing automatic and helping retirees spend what they had saved more confidently.

NYC-headquartered BlackRock is the world’s largest asset manager, with $10 trillion in assets under management as of January. It grew from startup to industry leader status in less than 40 years and, according to Fink’s letter, more than half of the assets it manages are for retirement.

[ad_2]

Source link

[1/5]Firefighters work at the scene following a fire in a retirement home in Milan, Italy, July 7, 2023. REUTERS/Claudia Greco

MILAN, July 7 (Reuters) – An overnight fire in a retirement home in Milan killed six people and injured around 80, including three who are in a critical condition, Italian authorities said on Friday.

The fire started in a first-floor room of the facility. It was put out quickly and did not spread to the rest of the building, yet produced a vast quantity of toxic fumes.

Two residents burned to death in their room, while four others died from intoxication, Milan Mayor Giuseppe Sala said, speaking to reporters on the scene.

“It could have been (even) worse. Having said that, six dead is a very heavy death toll,” Sala said, indicating that the facility housed 167 people.

Firefighters’ spokesman Luca Cari said the cause of the fire was under investigation, but added that it was likely accidental.

Firefighters intervened at the “Home of the Spouses” residential facility in the south-eastern Corvetto neighbourhood shortly after 1 a.m. (2300 GMT).

They evacuated about 80 people, including many in wheelchairs, while another 80 or so were taken to hospital, local firefighters’ chief Nicola Miceli told RAI public television.

He described rescue operations as “particularly complicated” due to heavy smoke, which limited visibility, and the fact that many residents could not stand without aid.

Lucia, a local resident, said she saw some of them “gasping for air” at their windows, holding rags over their faces to protect themselves from the fumes.

She said rescuers “were wonderful” as they helped everybody. “Those who could walk, they walked them out, those who could not, I think they were carried out in their bed sheets.”

Additional reporting by Giselda Vagnoni, editing by Keith Weir

Our Standards: The Thomson Reuters Trust Principles.

[ad_2]

Source link

Raising a child, especially in the current US economy is an expensive affair. Thousands go into education, healthcare, and fulfilling basic day-to-day needs. Hence, a lot of times, couples don’t save enough for their retirement and end up depending on their children to finance their retirement plans. But is that really a good idea? Absolutely not!

Not only is it unfair to your kids, but it’s also risky to give up your financial freedom and rely on someone else for every dollar you need. So how exactly should you be planning your retirement? Read till the end to find out.

6 reasons why your children shouldn’t be your retirement plan

While it’s common in some cultures to rely on your children to fund your retirement, it’s a bad move from a financial point of view. Here are six reasons why you shouldn’t rely on your lids for retirement:

1. They might not always be there

While no parent wants to imagine their children dying before them, there’s always a possibility that you cannot ignore. God forbid, but if something like this were to happen, you’ll not only lose your child but also your means of survival.

Just imagine, if you were to die at 60, your kids could still go on without you. They would be done with college by then and be happily settled in a stable career. But if you’re left alone at 60 with no retirement fund, you can neither join back the workforce nor start a business of your own (since you don’t have the capital). Frankly, it would be over for you.

2. You might miss out on a lot

When you depend on someone to fund every part of your life, they only take care of your needs, not your wants or dreams. For instance, your child might be happy to put a roof over your head and provide you with warm meals and other basic necessities. But they surely can’t fund your dream world tour with your spouse or the car you’ve always wanted.

For most people, retirement is a way to get back everything they missed during their younger days when they were busy hustling and grinding to raise a family. But the only way to get back the dreams you left in your youth is through sufficient funds. Otherwise, all those years of hard work will yield nothing but a boring and unfulfilling retired life.

3. It can lead to internal conflict

Setting aside family values and emotions, raising a family on a single income is tough. Prices of everything, be it basic daily needs or luxuries such as properties are at an all-time high. In a situation like this, it can be very hard for your kids to run their families as well as look after you and your spouse. And whether you like it or not, it might lead to internal conflict.

So instead of risking your relationship with your children and adding to their already overflowing plate of responsibilities, taking care of your own finances, even post-retirement, is a smart move. They’ll be more than welcome to contribute if they want, but imposing your financial needs on them will never work out.

4. You’ll be dependent

For someone who has worked their entire life and paid all their bills with their hard-earned money, it can be a little hard to give up all your freedom and rely on someone else, even if that’s your own child.

They might not mind supporting you, but they might require accountability. Think about it, after being financially independent for decades, can you really go back to telling someone why you need $100 or how you intend to spend it?

Not to mention, your kids might not be thrilled with the idea of supporting you throughout. After all, there have been countless instances where old parents have been abandoned by children.

Sure, you might not think that your kids will do that to you. But do you really want to take that risk? Remember, it’s hard to start over with a new career at 60, especially if you don’t have enough funds.

5. It’ll hinder their financial growth

Just like we mentioned before, raising a family on a single income in this economy is challenging. On top of that, if they have to take care of you and your spouse, too, it’ll be impossible for them to grow financially.

All they make at work will directly go into rent, school fees, food, and other basic necessities for the family. By the time all the bills are paid, they won’t have enough left to save, let alone invest.

In simple terms, by expecting your child to pay for your lifestyle post-retirement, you’ll be capping their growth. They might be able to pay for their needs but achieving dreams and luxuries will be next to impossible.

6. Increased risk of poverty

Life might not have seemed so hard when you had your own money to look after your partner and home while all that your kids had to worry about was paying their own bills. But the moment you lose your income and the burden of all the bills falls on one paycheck, you’ll notice that slipping under the poverty line is easier than it looks.

It’s quite simple if one paycheck that was earlier used only to cover 1 or 2 people is now providing for four people, your standard of living and purchasing power will have to take a hit. In this case, your family will be the only major crisis away from falling into quicksand-like poverty.

Avoid these 3 mistakes to childproof your retirement plan

Let’s say you have planned the perfect retirement plan for you and your spouse. But does that guarantee stability? Not if you have dependent children. Here are three pitfalls to look for when planning for the future:

1. Plan your retirement saving as you plan your child’s college fund

The biggest financial contribution any parent has to make to their child is the college fund. Just like healthcare, education too is extremely costly in the USA.

So for starters, if you don’t have the fund to provide for both your child’s college and your retirement, prioritize the latter. You can always take an education loan for your child’s future, but you cannot request a loan for your retirement.

Also, try to help your kids earn more credit points, choose the right college, and land scholarships so that they graduate with lesser debt. Your kids might not like the pressure of paying off debt from the first day of their work life, but it’s still a better choice than depending on them for every small need for the rest of your lives.

2. Teach your kids to be financially independent

The sooner your kids will be financially independent, the more you can save for your retirement. Although many students manage to land a job after high school or college, having a job isn’t the same as being financially independent. It’s not uncommon to see adult children with jobs relying on their parents for additional support.

So from a very young age, teach your children to budget. The best way to do so is by providing them with a monthly allowance to manage their personal needs.

If your kid has never had any money of their own, they’ll be tempted to spend their money the moment they get a paycheck. However, if your kids know the value of money, how to manage all bills within a given limit, and the essence of saving, you won’t have to deal with reckless adult children who continue to rely on you for their basic needs.

3. Set limits on financial support for adult children

As a parent, it’s naturally difficult for you to see your kids in distress. But it’s important to keep your emotions aside and cap how much financial support you’re willing to provide to your adult children.

Life is full of ups and downs. They might hit a rough patch and lose their job, get divorced, or move back to your house. However, it would be unwise to spend your entire retirement fund on helping them get back on their feet because once they do, they’ll go on with their lives while you’ll be stuck penniless in your 70s.

Also, if you help your kids every time they’re in trouble, they’ll never learn how to manage their crises on their own.

So for the benefit of both parties, it’s best to limit your spending on adult children. Let them figure out their lives on their own so that you can have enough to live comfortably with your spouse till the very last day.

Best retirement plans & schemes to secure your future

Not everyone in the USA has access to employer-sponsored retirement plans. And even if you do, it might not be enough for the life you’re planning ahead. In that case, here are some long-term retirement plans for you and your spouse to secure your future.

1. Traditional IRA

The easiest retirement plan is to go through a traditional IRA. This plan works for anyone who has a taxable income but doesn’t have an employer-provided pension. Under the IRA, you can choose where to invest your money. It could be mutual funds, ETFs, and other assets. The amount you pay to the IRA is tax-deductible, and your income from those investments is also tax-free.

However, once you start withdrawing your funds after the age of 59.5, your earnings will be taxed just like regular income.

2. Spousal IRA

The spousal IRA isn’t technically an individual type of IRA. It’s more like a way to maximize your retirement savings. This plan is perfect for couples where one partner is either unemployed or makes significantly less than the other.

Under this plan, the working partner can contribute to the IRA account of the non-working partner. Since the fundamental rule of IRA requires the person to have an income in order to contribute, a spousal IRA is a perfect solution for dependent partners.

3. Roth IRA

Roth IRA offers the perfect retirement plan for those families that don’t have a high annual household income. Unlike a traditional IRA, the amount you deposit here won’t be tax-deductible, but once you retire and finally start utilizing the fund, you won’t have to pay a single penny in tax.

On top of that, Roth IRA can also double up as your emergency fund because it lets you withdraw funds before retirement without a penalty.

4. Traditional 401(k)

This plan will work only if an employer provides a 401(k) account to you. Under this scheme, you’ll be putting in a part of your pre-tax income all the way until retirement. Since these investments are made on a tax-deferred basis, you won’t be taxed for the returns on your investment until you start withdrawing from it.

Some employers also encourage their employees to invest in 401(k) accounts by matching their total investment up to a certain percentage of their salary.

5. Roth 401(k)

A lot of employers offer Roth 401(k) along with traditional 401(k). The only difference is that for a Roth 401(k) account, the income comes from your after-tax salary (unlike a pre-tax salary, as in the case of traditional 401(k) accounts).

In addition to that, the income you make from those investments is not taxed, even when you start withdrawing them post-retirement.

The trick to picking the right plan is to check in which scenario you’ll be paying lower taxes. If your income tax is lower now, but all these investments can land you in a higher tax bracket, go for the Roth 401(k) plan

6. Solo 401(k)

This is the perfect retirement plan for self-employed individuals. Under this scheme, you contribute to your 401(k) account both as an employer and an employee, enabling you to maximize your retirement savings.

As an employer, you can contribute up to 25% of your total compensation, and as an employee, you can contribute up to $66,000 or $73,500 (if you’re over 50) to the fund. Just make sure that the total contribution doesn’t exceed $66,000 or $73,500 if you’re over 50.

Conclusion

There’s no doubt that you love your children, and they love you too. But it’s best to let practicality take the lead when it comes to finances. The number one rule of finance management is to prepare for the future.

A part of the money you earn today should go into securing the days you don’t have an income, and relying on your kids is certainly not the best way to go about it.

We hope our guide was able to show you the right way to a happy and secure retirement. Feel free to check out more such guides on our website to know all there is to know about managing finances for and post retirement.

The post Are Your Children Your Retirement Plan? appeared first on Due.

[ad_2]

Source link

Jim Cramer’s approach has always been practical and positive about financial freedom after retirement. He runs the CNBC investing club, which helps people make worthy investment decisions to amplify their money. In addition, Cramer is the co-founder and chairperson of TheStreet.

Born to creative parents, Cramer has always been appreciated for his unique ability to provide logical financial suggestions. Do you know what Cramer says about early retirement? This post unveils the secret – keep reading and learn the mysteries involved!

Cramer’s Take on Early Retirement

Jim Cramer published a book called “Real Money‘ in 2005. On page number 66 of the said book, Cramer said – “the age-specific investment approach is your best option.” These lines reflect how crucial it was for Cramer to save for retirement. He believes everyone should start saving for retirement as early as possible.

Cramer started his career with the Tallasahi democrat. In 1977, he got his first steady paycheck. However, when he left Talasahi, he passed through tough times. He was living in his car when he used to work as a reporter in Los Angeles. Impressively, dodging that adverse financial situation, Cramer managed to put $1500 away for his retirement.

He says he invested the money in the famous Peter Lynch at Fidelity Magellan Fund. According to Cramer, that money was being invested for multiple years consistently. This, in turn, helped him to compound the money to such an extent that it could provide a moderate retirement income to live lavishly for at least a half dozen years post-retirement.

In the dawn of 2023, Cramer’s ideology seems very relatable. Saving for retirement has never been this crucial – the job market has gone insanely unstable, and the economy craves oxygen because of inflation. This is high time to adopt an age-specific mindset, as Cramer explains – you should focus on growth stocks in your 20s because you have enough time to take and manage risks.

When you enter your 30s, you should pull the chain a little hard and switch to more stable stocks like dividends. Moving on to your 40s, bonds should make up a more significant portion of your portfolio since this is the time to prioritize capital preservation.

According to Cramer, given the disrupted economic scene in the USA, even highly curated plans for retirement may fail. Therefore, you should switch to the alternative of retiring early. However, how should you move towards early retirement?

How Should You Plan for Early Retirement?

Cramer articulates that sticking to a strategy from your early 20s may help you retire early and enjoy financial freedom. There are several elements to consider, including the following.

1. Know Your Style

When you are beginning, it’s crucial to know where you stand. Ideally, you will need 70% of your yearly income to fuel your yearly expenses after retirement. Therefore, identify your present financial position and look for ways to secure that percentage so you can retire early and not see poverty post-retirement.

2. Focus on Compounding

Only compound interest can grow your money substantially. If you want to estimate how quickly you can multiply your money, you just need to figure out the years needed to grow it at a given interest rate. For instance, if the interest rate is 10%, it will take approximately seven years to grow $1000 into $2000. If you want more benefits, you can consider high-yielding stocks.

3. Set Realistic Goals

Be realistic when carrying out the calculation. If you are retiring early, you will probably live a long time without work. Is the venture going to be riskier than you bargained for? Will you be able to manage enough money to enjoy your retirement? Reassess the factors before you say goodbye to your job. Remember, leaving your retirement entirely on double-digit investment returns is not wise. Hence, be careful!

4. Don’t Ignore the Health Factor

Everything about retirement may not be that juicy. You may experience health issues that can make a big hole in your pocket. Therefore, get health cover that can help you with your hospital bills.

5. Choose the Right Investment Vehicle

If you have decided to retire early, you are probably ready to compromise the comfort of your monthly salary. Therefore, you should utilize the limited time frame to save massively for your retirement years. For instance, if you started earning at the age of 18 and you are planning to retire in your 40s, you will have approximately 20-22 years to grow your money and save for your retirement.

Given this, you should be very particular when picking investment instruments. Always walk with the alternatives that ensure sizeable returns over time. Besides, they should be able to beat inflation. You can browse through equity-based alternatives or annuity plans to secure a regular flow of income.

6. Manage Your Portfolio Sensibly

Only consistency can help you reach your goal when it comes to retiring early. Therefore, be regular with your investment and manage your portfolio actively. If you truly want to maximize your returns, consider monitoring your investments closely. You should be able to figure out which investments will suit you and which won’t.

The investments you have made previously should also be reanalyzed. Check if they hold their ground in the present day and have helped combat inflation. If their performance doesn’t seem promising, take out your money and put them in the right instruments.

7. Calculate your Requirement

You can do this by referring to the rule of 25. This says that you should acquire 25X your planned annual spending before retiring. For instance, if you want to spend $40,000 during the first year of retirement, you should have $10,00,000 invested when you leave your job. When you invest your retirement nest egg, it will continue to grow. This way, they will be able to keep up with the inflation.

8. Know the 4% Theory

The 4% rule is a widely accepted idea for retirement planning. It suggests that you can withdraw 4% of your invested savings during the first year of retirement. Afterward, you can adjust the withdrawal amount for inflation every year. Although you don’t have to adhere strictly to the 4% rule, you can make adjustments based on your risk tolerance, market performance, and investment portfolio.

9. Use Low-cost Index Funds

Retiring early comes with two clear downsides – a shorter span to save and a longer period to spend. You need to achieve the best returns to dodge them, which can be done by building a balanced portfolio inclined to long-term growth. You can use low-cost index funds to achieve this goal. Usually, such funds come with allocations tilted toward stocks, and you are free to stomach them as long as you can.

10. Expense Check is Mandatory

Well, you may have done loads of homework to figure out how much you will need to spend your retirement comfortably. However, estimating the expenses could be a discussion. Generally, it starts in an innocent way – you throw that mandatory retirement party. After a few days, boredom hits, and you go out for a vacation. Then, you need a companion, so you get a dog. Well, now the 4% rule, as mentioned above, suddenly kicks in.

You should avoid this scenario. You decided to stick to that rule to beat inflation. It can never help you if you mindlessly spend much beyond your capacity. If you increase your recurring expenses in your retirement, you will likely run out of money soon.

11. Avoid Debts

Debts can be a hindrance to your early retirement efforts. When you are stuck with debt, you will find it challenging to acquire enough money to support your post-retirement life. Ideally, you should follow the fundamental 30:30:30:10 budgeting rule to avoid financial burdens.

As such, you should dedicate 30% of your monthly income to housing needs, 30% to groceries, utilities, and fuel, 10% to discretionary expenses, and 30% to your savings and investments. By following this rule, you will be able to save in a strategic and disciplined way.

12. Consider Passive Income

Building a passive income stream may help you retire early, and there are several ways to do so. For example, you can start taking up freelancing projects or invest in dividend assets. Besides these two, you can also consider several other ways to generate passive income. They may include real estate investing, affiliate marketing, and creating and selling digital products. The key is to find a method that works for you, and that aligns with your financial goals.

Facts About Early Retirement That You Shouldn’t Ignore

Now that you are familiar with the secrets of early retirement, here are some lesser-known facts that can help you make an informed decision. Remember, everything about retiring early is not sweet, and you should be prepared to embrace its bitter side as well.

1. Unpredicted Spending

As highlighted before, in retirement, you will typically need to spend only 70% of what you spent when you were working. For example, if you spend $10000 yearly when working, it is expected to become $7000 once you retire. There won’t be liabilities such as shoveling money into your retirement account, paying social security taxes, and bearing the communication cost for work. However, in the early years of retirement, you are expected to spend more than you planned to fuel your newly retired lifestyle.

Moreover, the inflation rate is running at a red-hot 8.3% now. Nobody can say it will surge to what extent when you retire. Given this, you may need to revise your retirement savings plan considerably. EBRI reveals that 36% of retirees agree that their overall expenses have been higher than their calculations. Considering these facts, you should start saving even more rigidly to spend your retirement in comfort and peace.

2. Elevated Costs

Sometimes tapping your nest egg early may cost you significantly. Retiring before 59 makes you likely to pay a 10% early withdrawal penalty from tax-deferred accounts like 401 (K) plans and IRSs. Moreover, if you don’t have a Roth IRA, funded with after-tax contributions, your withdrawals from traditional accounts will be subjected to tax implementations.

For instance, if you withdraw $40,000 before you hit 59 and come under the 15% federal tax bracket, you are expected to pay $10,000 in penalties and taxes. This will leave you with $30,000 in hand.

3. Burdensome Housing Expenses

If you are retiring with a mortgage, your housing expenses won’t retire with you. Thus, you should always try paying off your mortgage before you say goodbye to your job. However, even if you manage to pay your mortgage, you should be careful about your property taxes and home maintenance costs and plan your retirement budget accordingly.

FAQs

1. What happens if you retire early?

Retiring early comes with a set of pros and cons. The benefits may include several elements. For instance, you can enjoy an opportunity to start a new career. Furthermore, early retirement allows you to spend more time traveling and exploring different dimensions of life. Most importantly, if you have planned strategically, early retirement can help you cherish financial freedom.

However, there are downsides as well. First, your social security benefits will be reduced. Next, you may struggle to make your retirement savings last longer. Finally, the lifestyle transition may affect your mental health.

2. What is the ideal age to retire?

Well, the answer is pretty self-explanatory. Most people believe the standard retirement age should range between 60 and 65. In fact, if you retire at this age, you can draw your full social security retirement benefits. However, depending on your financial situation, you may decide to retire early or late. There is no definitive formula that can help you find the right age for retirement. Thus, consider your goals when making the decision. You can also take professional help from financial advisors to make the right decision.

3. How can you comfortably prepare for early retirement?

To set yourself free before you hit your 59, you must plan your finances strategically. You should invest in the right instruments, keep track of your budget, and save adequately for your future. In addition, you should purchase health coverage to deal with unforeseen medical emergencies.

4. Should you retire early?

Yes and no! If you plan to start a new venture after your 40s and your job obstructs your way, you may consider the idea of early retirement. Similarly, you can retire early if you want to enjoy a burden-free life a little earlier than the standard norms. However, if you are burdened with loans and have not been able to manage your finances well so far, you should think thoroughly before deciding to retire early.

5. What did Cramer say about early retirement?

Jim Cramer has always been positive about the idea of early retirement. In fact, he considered it one of the best weapons to beat inflation and live a worry-free life. However, Cramer has recommended a few to-dos to obtain the best benefits of early retirement. They include strategic and consistent savings, awareness of the present financial condition, etc.

The post Jim Cramer’s Secret to Early Retirement is Now Public appeared first on Due.

[ad_2]

Source link

You can help your relatives immensely by setting up an estate plan now, regardless of who you are. Essentially, whatever you own makes up your estate. These assets could be:

- Any property your own

- Whatever money you have in a bank account

- Stocks, bonds, and mutual funds invested through a taxable brokerage account

- A Roth IRA

- Your prized vinyl, stamp, coin, or art collection

Having a say in how your estate is distributed is essential to your estate planning. Although it may seem daunting, saving your loved ones thousands of dollars will likely be worth the effort now.

In short, you and your family can benefit from estate planning regardless of your net worth.

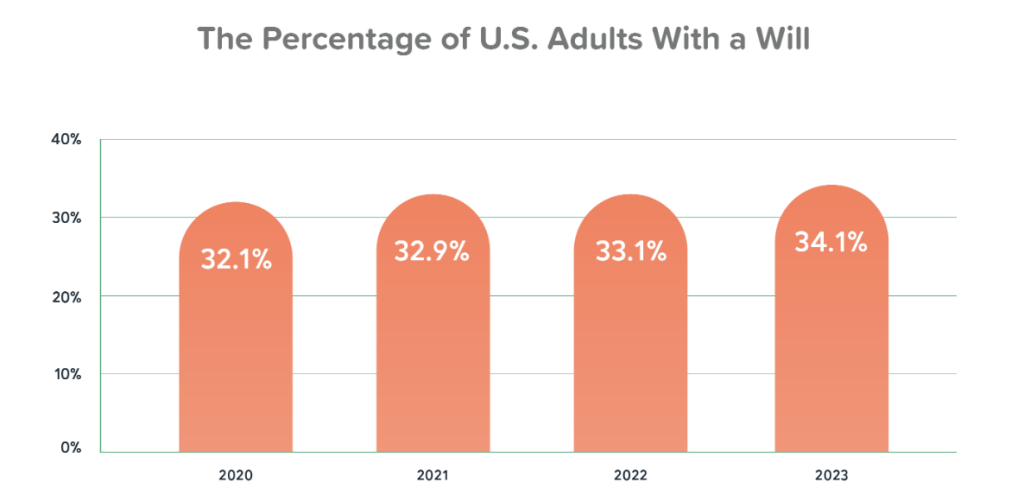

Despite this, 2 out of 3 Americans do not have any type of estate planning document, according to a survey conducted by Caring.com.

“Estate planning is one of the crucial elements of a comprehensive financial plan, but somehow is also the most overlooked component, with the majority of adults not having any form of estate planning document,” says Patrick Hicks, General Counsel and Head of Legal at Trust & Will. “Having an estate plan is a continuation of financial planning and essential to ensure that your efforts to provide for your loved ones last into the future and act as a foundation to build multigenerational wealth and leave a legacy.”

What is Estate Planning?

In essence, estate planning is deciding how you want to distribute your assets after you die — or become incapable of making financial decisions for yourself. If you have trouble putting together an estate plan, and have the funds, consult a financial adviser and a lawyer.

Again, whether you’re broke or not, an estate plan is essential. Even though estate planning may seem morbid, it has several advantages:

- Your wishes will be legally binding when deciding who gets your assets.

- In order to minimize your estate’s tax burden, you can arrange it in a way that minimizes taxes.

- The peace of mind of knowing that your financial affairs are in order means that your loved ones won’t inherit an administrative nightmare.

There are several elements to an estate plan, including:

- A will.

- Having someone you name to manage your finances if you are unable to do so is called an assignment of power of attorney.

- An advanced directive, also called a living will, expresses your wishes for life-sustaining medical interventions if you are terminally ill or incapable of communicating for yourself

- You can give someone you trust the authority to make medical decisions in your name by using a healthcare proxy.

There are some people who might benefit from a trust as well.

Estate Planning Checklist

Make an inventory.

Your possessions might seem insufficient to justify estate planning, but you may be surprised at just how much you actually have. As such, keeping track of your tangible and intangible assets is easy with an inventory.

Estates may contain tangible assets such as:

A person’s estate may contain the following intangible assets:

If you have outstanding liabilities, you should also list them. These are any debts that have not yet been paid in full like mortgages, credit cards, or other debts. If you die, an executor of your estate can notify creditors more easily by keeping a written record of your outstanding debts.

Prepare your estate plan.

Answer these questions about how to settle your affairs before meeting with an estate planning attorney:

- How should your assets be distributed to your heirs?

- If you have minor children, who should care for them?

- What is the cost of caring for and educating your children?

- During an illness or injury, who should manage your financial affairs?

- When it comes to distributing your assets, who should be in charge?

Decide what your directives will be.

Legal directives are an important part of an estate plan. These typically include:

A trust.

Your assets are placed in a trust for your benefit (and that of your beneficiaries) and managed by a trustee. Your trustee can take over if you become incapacitated or ill. When you die, the trust assets are transferred to the beneficiaries of your choice, bypassing probate. Alternatively, you can create an irrevocable trust, which cannot be changed or revoked.

Living wills are also known as medical care directives.

In the event that you become incapable of making medical decisions for yourself, it outlines your wishes for medical care. If you are incapable of making health care decisions, you can also give a trusted person medical power of attorney. Advance health care directives combine these two documents into one.

Power of attorney for financial matters.

When you are medically incapable of managing your financial affairs, someone else can. It is your designated agent’s responsibility to act on your behalf in legal and financial situations when you are unable to do so. In addition to paying bills and taxes, they’ll also be able to access and manage your assets.

Power of attorney with limited authority.

You may benefit from this if you feel uncomfortable about turning everything over to someone else. Your named representative’s powers are limited by this legal document. During the closing of a home sale or when selling a specific stock, you could grant the person authorized to sign the documents on your behalf.

Don’t give your power of attorney to just anyone.

Your financial well-being – or even your life – might be at their disposal. In case your primary choice is unavailable, you might want to assign medical and financial representation to different people.

Almost all states offer standardized forms for medical powers of attorney that can be filled out in the blanks. It is not uncommon for states to provide a form for financial power of attorney, as well as a living will or advanced directive.

Forms generally won’t cost you anything, but notarizing them will. There are different notary fees in different states, ranging from free to $25.

Your beneficiaries need to be reviewed.

Although your will and other documents may outline your wishes, they may not cover everything.

- Keep an eye on your retirement accounts and insurance policies. You need to keep track of beneficiary designations on retirement plans and insurance products. Beneficiary designations usually take precedence over wills.

- Make sure your stuff gets to the right people. The names of beneficiaries on policies and accounts established many years ago are sometimes forgotten. A life insurance policy that has your ex-spouse as a beneficiary, for example, might not pay out to your current spouse after you die.

- Be sure to fill out all beneficiary sections. During probate, an account may be distributed based on the state’s rules for distributing assets.

- Specify contingent beneficiaries. Having backup beneficiaries is essential if you forget to update the primary beneficiary designation and your primary beneficiary dies before you do.

Make sure you know the estate tax laws in your state.

It is often possible to minimize estate and inheritance taxes through estate planning. However, most people will not pay these taxes.

Only estates exceeding a certain amount are subject to estate taxes at the federal level. It generally applies to assets valued over $12.06 million in 2022 or $12.92 million in 2023 and has a tax rate of 18% to 40%. What if your estate exceeds the federal limit? Your heirs may benefit from a grantor-retained annuity trust, also known as a GRAT, which is an irrevocable trust.

Additionally, estate taxes are imposed in some states. If an estate’s value is below the federal government’s exemption amount, then the state may levy an estate tax. There are also inheritance taxes in some states. As a result, those who inherit your money may have to pay taxes

Consider the value of professional assistance.

In general, your situation will determine whether you need to hire an attorney or estate tax professional to help you create your estate plan.

- In the case of small estates and simple wishes, an online or packaged will-writing program may suffice. You will usually be guided through writing a will using an interview process about your life, finances, and other bequests, in accordance with IRS and state requirements. Your homemade will can even be updated as needed. Compared to working with an attorney, online wills are less expensive. With LegalZoom, you can create a simple will for $89, a comprehensive will for $99, and an estate plan package for $249. Nolo’s Quicken WillMaker and Trust lets you create over 35 documents ranges from $89 to $199.

- Getting legal and tax advice may be worthwhile if you have doubts about the process. When you live in a state with its own estate or inheritance taxes, they can help you determine if you’re on the right estate planning track. A will and powers of attorney can cost as little as $1,000. But a complex estate will require you to work with an attorney. The cost of hiring a lawyer can range from $100 per hour to $400 per hour or more.

- An estate attorney or tax professional can assist in navigating the sometimes complicated implications of a large and complex estate – such as childcare concerns, business issues, or non-familial heirs.

Maintain a current estate plan.

Keep your estate plan updated once it has been finalized. According to Bob Carlson, senior contributor to Forbes, paperwork should be reviewed every three to five years. Your estate needs to be reviewed and revised if you experience major life changes, such as:

- When a child is born, adopted, or dies

- Marriage, divorce, or separation

- Whenever you move to a new state

- A major income change has occurred

- Whenever the tax law has been significantly changed

FAQs

1. What is estate planning?

In estate planning, you work with professional advisors who know your goals and concerns, your assets, and how your family works. It might involve lawyers, accountants, financial planners, life insurance advisors, bankers, brokers, and more.

Tax planning may or may not be involved with estate planning, which involves transferring assets at death. Wills are the most common documents associated with this process.

2. Do I have an “estate”?

When someone dies, their estate is everything they own before they’re distributed by will, trust, or intestacy. An estate can have real property, like houses, as well as investment properties. It also includes personal property like bank accounts, stocks, jewelry, and cars.

3. What’s the point of planning?

An estate plan lets you decide who gets what from your estate, and how much. In addition, it prevents taxes from ruining the estate.

4. Is a will necessary?

No. Wills aren’t required by law. However, most people should make a plan for how their finances and property will be divided after they die.

For starters, you can control how your assets are distributed when you die by making a will. In the event you pass away without a will, you won’t be able to choose what happens to your stuff. Your will lets you decide who gets what, or whether certain people aren’t allowed to get anything. This is called disinheriting an heir. In many cases, naming the person who will wind up your affairs makes all the difference in how smoothly things go. Knowing they’ve picked someone they trust to handle their final affairs gives people peace of mind when they make a will.

Also, in an unfortunate scenario where you pass away while your children are still minors, a will lets you plan for their care. Plus, a will can save your heirs the trouble of going through probate. You can also avoid estate taxes by making a will. Your beneficiaries and heirs won’t have to pay estate taxes on the amounts you left them.

Wills aren’t permanent, so you can change them anytime. In case you decide to divide your estate differently later, you can make any adjustments you need.

5, What happens if I don’t have a will?

Without a will, your property passes according to state law, regardless of what you want. A person dying intestate means they die without a legal Will, and intestacy is what happens to their estate without one.

In most cases, the estate of a married person who dies with a spouse still alive goes to the spouse. If you don’t plan ahead, your surviving spouse can use your assets, savings, and retirement to support his or her new family.

A person’s spouse and children from a previous relationship are usually exceptions. A surviving spouse usually gets one-third of the estate if there’s no Will, and two-thirds goes to the children. Wills are needed if a person wants their assets disposed of differently than by statute. You can add a lot of stress and expense to an already emotional and difficult situation when you die without a will.

The good news? Wills don’t have to be complicated or expensive.

The post Retirement and Estate Planning for Broke Individuals appeared first on Due.

[ad_2]

Source link

The U.S. has gone through massive crises that put a lot of households and businesses at rock bottom. It’s been over a decade since the Real Estate Bubble and the Great Recession. Yet their impact has been unforgettable. These are only two unforeseen events that sparked a surge of bankruptcies. And roughly a year before the pandemic, millions of Americans struggled to recover.

In 2020, the pandemic crisis transpired and scourged the U.S. economy. The restrictions led to limited operations across industries and overwhelming cash burns. In turn, millions of businesses had to shut down, either temporarily or permanently. It was most evident in the SME sector, with 9.4 million small businesses closing that year. Although the recession only lasted two months, the road to recovery was long and winding.

In the last two years, the economy has demonstrated a strong rebound. Thanks to easing restrictions that allowed business reopenings and increased operating capacity, unemployment was lowered, and the pent-up aggregate demand was fueled. At the end of 2021, GDP per capita reached $12,235, a 12 percent year-over-year growth. It even exceeded pre-pandemic levels with $11,300 on average.

Today, the U.S. is again facing a threat to its economic recovery. Inflationary pressures have stretched further than expected, peaking at 9.1 percent in 2022, based on a post published in Trading Economics. In response, the Fed made a series of interest rate increments peaking at 75 basis points. The effort is now paying off as inflation relaxes to 6.5 percent. However, one must not be complacent as rates may keep increasing to ensure macroeconomic stability.

Given all these factors, the labor market demographics have transformed. Retirement age is increasing along with prices. It is no surprise many would-be retirees are delaying their retirement. In fact, more than half of female workers decided to extend their working years. This is a logical choice since there are fewer revenue streams upon retirement. The last thing retirees need is cost-of-living adjustments.

Thankfully, they can get through life amidst market volatility. This article will discuss how retirees can cope with the impact of rising inflation.

Inflation Before and During the Pandemic

Inflation has always been one of the integral macroeconomic indicators in the U.S. economy. It has played a vital role in gauging economic performance and predicting crises in the last century. In fact, economists built theories that put inflation at the center. One of these was the Phillips Curve. Analysts observed inflation’s increased predictability after WWII and the Korean War.

In the following years, the Fed thought they had a grasp on inflation. They tried to use its impact on the unemployment rate. However, this was disproven after the sustained high inflation led to stagflation. In the early 1980s, it was further proven to be meaningless as another massive crisis took place. Since then, the Fed went back to basics as interest rate adjustments remained effective. The inflation rate had become more stable and moved in a downward pattern.

In 2008, the Great Recession put millions of Americans into the gutter. Various factors contributed, but the real estate bubble was the primary driver. The effects of inflation were most evident in the commercial and residential property market. From 1996 to 2007, house prices rose by 124 percent. Even worse, the ratio of home prices to median income rose from 3:1 in 2001 to 4.5:1 in 2006.

People believed that real estate appreciation would continue, which encouraged adjustable-rate mortgages. But the lenders failed to account for the borrowers’ capacity to pay. By 2007, lenders had 1.3 million properties in foreclosure proceedings. And by 2008, home prices plunged by 20 percent.

Inflation effects on other industries should also be highlighted. The beginning of the recession was characterized by inflation rising above 5 percent for the first time in almost 20 years. In response, the Fed raised interest rates to help the economy cool down. It proved effective, but it led to contraction across industries.

Higher production and borrowing costs forced companies to lay off employees or shut down. In turn, the unemployment rate reached a new all-time high. The Bureau of Labor Statistics showed it peaked at 10 percent in 2009. This unprecedented event depleted the savings of millions of Americans. Retirees were the most affected and forced to delay retirement or return to work.

In the following years, the U.S. economy tried to regain its footing. Although the recession ended in 2009, the effects of inflation and interest hikes, unemployment, and the housing crash persisted. It was only in 2014 that the unemployment rate returned to pre-recession levels. Analysts also became wary of another potential recession in 2015. The U.S. economy slowed down once again, although the global economy was far more sluggish. Thankfully, it quickly recovered, with the GDP growth rate rebounding to three percent. Median household incomes also bounced back to pre-recession levels in 2016.  Amid all these massive changes, we can identify one important thing. Inflation has not played by the rules since the aftermath of the Great Recession. For instance, the Fed has implemented expansionary monetary policies to stimulate activities. Yet inflation was of little concern as it remained within the two percent target. By 2018, the U.S. recovered as the GDP growth rate became more stable.

Amid all these massive changes, we can identify one important thing. Inflation has not played by the rules since the aftermath of the Great Recession. For instance, the Fed has implemented expansionary monetary policies to stimulate activities. Yet inflation was of little concern as it remained within the two percent target. By 2018, the U.S. recovered as the GDP growth rate became more stable.

In 2020, the U.S. faced another recession when the pandemic hit. Pandemic restrictions led to limited operating capacity and net losses. They led to massive layoffs and business shutdowns. The stock market prices dropped instantaneously, although the rebound immediately followed. Meanwhile, inflation fell to 1.24 percent as the demand across industries dropped. The unemployment rate set a new all-time high at 14.7 percent, as shown by the Bureau of Labor Statistics. In response, the Fed set interest rates to near-zero levels to attract business spending on investments and borrowings. All these events showed that inflation once again played by the rules.

Rising Inflation Today

Despite the pandemic restrictions, the U.S. economy found ways to withstand blows and bounce back. The third quarter of 2020 showed a slight recovery as businesses began reopening, thanks to digital transformation that empowered cashless transactions, hybrid work setups, and e-commerce. Also, the pent-up demand across industries contributed to business reopenings. Therefore, in 2021, labor market conditions improved as unemployment decreased by 4.1 million.

The market improvement was most evident in real estate. When interest and mortgage rates dropped, more prospective property owners applied for loans. The expected property appreciation also drove this scenario. As such, home sales soared and set the highest record in 14 years. In other industries, business reopenings increased as production costs and restrictions eased. The economy was poised for a strong and sustained rebound.

But only a year later, things seemed problematic for the U.S. economy. The Russo-Ukrainian War further aggravated the situation. Inflation is rising above pre-pandemic levels and stretching further than expected. In 2022, it reached 9.1 percent, a new record high in over 40 years. Fuel prices have skyrocketed, leading to rising costs of production. This coincided with the clearing of supply chain bottlenecks. In turn, the softening of demand across industries sped up.

To stabilize market volatility, the Fed had to become conservative in raising interest rates. It made a series of interest rate hikes by 75 bps for four consecutive quarters. Fortunately, it proved effective by enticing more savings and limited borrowings and spending.

Today, inflation stays elevated but much lower than its 2022 peak. According to the same Trading Economics article, It continues to relax at 6.5 percent. The consumer price index (CPI) of 296.80 is also improving from the 2022 peak of 298.01. Although it is only a 0.5 percent decrease, we are more optimistic about the macroeconomic conditions this year. Inflation and CPI may keep decreasing as the Fed ensures stability.

On the flip side, analysts worry about another recession. But it may not be deep since the 2022 inflation was more of a demand-pull than a cost-push. This is normal due to pent-up demand amidst economic recovery. Market volatility has become more manageable since inflation has dropped nearly 30 percent. Also, continued interest rate increments are expected, but these may cool down as inflation goes into a lull. In fact, the Fed only set the Q1 2023 increase at 25 bps. In the second half, inflation may become more manageable.

Moreover, the current economic scenario differs from the Great Recession. There are various factors to consider, but this article will focus on the most obvious ones. First, property inventories remain low, so shortages persist even if sales cool down. We can attribute it to property builders remaining conservative after the Great Recession.

It seems as though they have not ramped up construction and leasing over the past decade. Second, lending policies are stricter regarding the borrower’s ability to pay. Third, there is no speculative mania in the capital market. Fourth, the Fed’s effort easily stabilized inflation. Lastly, the unemployment rate is still a far cry from the labor market conditions in 2008-2009.

Of course, cost-of-living adjustments may continue as the purchasing power of consumers remains low. Near-term economic projections remain bleak. But in 2024, the efforts of policymakers may start to materialize.

Retirees are Most Vulnerable to Rising Inflation

The U.S. economy has gone through numerous massive crises, and retirees have always been one of the most vulnerable groups to risks. In the aftermath of the Great Recession, 25 percent of bankruptcy filings came from Americans aged 55 and above. Most of them were still working at that time. Many retirees had to deplete their savings accounts, borrow from predatory lenders, or return to work.

Today, another threat is here to disrupt their wealth management. Although the current market volatility is less risky, retirees must stay on the watch. Inflation remains elevated, raising the standard of living in the U.S. Also, healthcare costs are rising due to the combined impact of the pandemic and rising prices.

Currently, healthcare costs per person amount to $12,530 versus $11,462 in 2019. These events prove the importance of retirement planning and a consistent stream of retirement income. Sadly, the past decade has not been enough for many retirees to gain their lost retirement savings.

A recent survey shows over 70 percent of Americans have savings accounts. But inflation effects have been hard to tolerate. Another survey shows that 30 percent of American seniors have no retirement savings. Meanwhile, only 27 percent have maximum savings of $49,999. Even worse, 70 percent of American seniors are stuck in debt quicksand. In the same study, almost two-thirds of them admitted to having moderate to high financial security.

Given all these factors, it’s unsurprising that many Americans rely on social security benefits. But with the increasing cost of living, the amount they receive may not be enough today. Note that the average life expectancy in the U.S. is 79, so retirement may last 13 years. Also, those at least 65 years old are more likely to get hospitalized. So even with Medicare, healthcare and assisted living costs may not always be coverable. These figures show that many would-be retirees will have to adjust to the increasing standard of living.

American Retirees and Would-Be Retirees Can Get Through Inflation

This year, the annual cost-of-living adjustment (COLA) to social security benefits is 8.7 percent. This is one of the highest increments in over 40 years. It aims to cover the rising cost of basic goods and services for retirees. However, living on fixed income streams can still be challenging when prices are exorbitant. Although inflation is easing, prices are staying higher than pre-pandemic levels. These circumstances may require retirees to consider these valuable tips to cope with market volatility and rising inflation.

Review and adjust your monthly budget

Whether a retiree or a would-be retiree, you must take some time to review your monthly budget and expenses. Doing so can help you determine what matters in your spending and increase savings. You may start by identifying your fixed and variable expenses.

Fixed costs refer to your constant expenses, which are part of your necessities or monthly expenses. These include water and electric bills, rent or mortgage, insurance expenses, and taxes. Rent and insurance expenses are most likely unadjustable. You can reduce your consumption to lower your water and electric bills. There are strategies and preparations to help you limit your taxes.

Meanwhile, variable expenses are those you can easily adjust. These include your spending on food, entertainment, and hobbies. Although food is a basic necessity, you can find ways to reduce your spending. For instance, buying less red meat or opting to have your food delivered instead of buying ingredients and cooking them. This is more efficient if you are living alone. This way, you don’t have to spend money on transportation, gasoline, and electricity. You can also limit your budget for groceries and decide what you often eat and use. Other variable expenses are optional, so you can limit your spending on them or avoid it altogether.

Review your expenses and identify those you buy the most. You may find ways to limit spending in those areas to restructure your budget plan. For easier calculation, add your fixed and variable expenses per month. You can average expenses in the last twelve months or focus on the most recent month.

Next, deduct the total amount from your monthly income. You are spending beyond your means if the difference is a negative value. It may push you to bankruptcy or debt quicksand. If the difference is a positive value, you are spending your income well. You can use the remaining amount to repay borrowings or add to your savings and emergency funds.

Protect Against Fraud

Aside from ensuring that you are spending within your monthly budget, seniors need to be aware of internet security. Economic downturns have shown to be linked to increased rates of online fraudulent activity. Given their healthy financial savings, trusting nature and the fact that American seniors are a growing group of internet users, they are an attractive target for scammers. The FBI has estimated that more than $3 billion is lost every year by American seniors in financial scams including romance scams, tech support scams and lottery scams. Internet awareness and protection is an increasingly important topic to discuss with senior online users. There are simple steps you can take to protect yourself:

- Check emails. Don’t open emails, download attachments or click links from unknown companies or addresses you have never corresponded with. If you have questions, contact the company directly through their website email address.

- Don’t share information. Do not give your credit card, social security or other personal information in an email, chat or over social media to an unknown person or company.

- Invest in security software. Protect your computer with anti-virus, security and malware software from a trusted cyber security company.

- Secure websites. Check the address bar at the top of your browser to see if a site is secure. The address will start with https if it is secure, make sure to look for the “s’ in the address.

- Do a search. Search for the contact information and offer that is being proposed to you. If others have been connected it is likely to be posted online as a scam.

Scams can happen to anyone. If you think that you have been a victim, make sure to call the local police, your bank (if money has been taken) and the FTC to report the scam. This can be devastating, impacting your savings, your identity and compromise your budget so make sure to take steps to prevent this from happening to you.

Adhere to an efficient investment strategy

Investments can be an excellent way to increase wealth. But without proper asset management, all your resources may go down the drain. As a beginner, you may put your money in a trusted brokerage and let them find the best asset classes. They will base it on your risk preference and tolerance. You can also go solo if you prefer to do things your way.

The bond market may be a perfect fit for you as a conservative investor. Although it has lower yields, its volatility is more manageable than the stock market. You must also understand that bonds do not go along well with higher interest rates. Typically, they have an inverse relationship. But since inflation is cooling down, interest rates may follow the trend in the second half of this year. So it may be an excellent time to buy bonds while they are still low.

To be more secure, you can go for treasury inflation-protected securities (TIPS). Tips are also bonds, but they are often government-backed securities. Also, they are more inflation-linked, helping them to hedge risks and valuation losses due to inflation. They have far better yields than the rest of the bonds amidst market volatility.

If you are more of a risk-taker, you can invest in stocks. They have higher risks, but yields are more promising. Also, you can be more secure while trading by choosing dividend-paying stocks. Price corrections may still happen as recession fears persist. As such, you must consider several factors before buying stocks. You can start by assessing their fundamentals. They will hint at the stocks’ performance and ability to sustain their operating capacity. From there, you can check the whole industry and compare how your preferred company performs relative to its peers. Lastly, assess their stock price, whether undervalued or overvalued.

Protect your wealth with insurance or annuities

Having savings and investments may not be enough. Crises and natural disasters have proven that anyone can deplete their wealth instantly. With that in mind, you may add an extra shield to your assets. Insurance and annuities are both excellent options.

Many reliable financial advisors offer insurance products and annuities. They ensure financial security for retirees by providing them with single or perpetual payouts. You only have to pay premiums to avail yourself of one and maintain your funds in your account.

For better understanding, insurance is a payout distributed upon the death of the policyholder. Meanwhile, annuities are a constant or single payout distributed as long as the policyholder lives.

Delay social security benefits

The current legal retirement age in the U.S. is 66. After filing your retirement, you can start receiving your social security benefits. However, delaying it is possible and even helpful in generating more social security income. You may increase your benefits for every year you delay your retirement or benefits up to 70. Therefore, if you wait for about two years, there may be a considerable improvement in your retirement income.

Talk with a financial professional

Retirement planning may be a long and winding process. It may be challenging, so you must prepare for it as early as you can. However, you must familiarize yourself with financial products before getting one. Check your budget priorities before saving. As such, talking with a financial professional can help you in wealth management and maintenance.

Learn More About Retirement Planning

Proper financial planning for retirement has become more crucial than ever for seniors. Market volatility has highlighted that your wealth can disappear in an instant. Therefore, a secure income stream can help you get through your retirement years. Having strategic investments, insurance, and savings will ensure adequacy. You can achieve your retirement goals with the right knowledge, no matter how complex retirement may be.

The post Rising Inflation: How Will Retirees Get Through Life appeared first on Due.

[ad_2]

Source link

Retirement Snapshot

Grant Sudduth in Bok Tower Gardens, Winter Haven, Florida

Photo credit: Tonja Sudduth

- Name: Grant S.

- Location: Frankfort, Kentucky

- Age: 69

- Retired At: 68

- Marital Status: Remarried

- Profession: Currently affiliate marketer/content creator; Retired from rehabbing homes

Grant’s retirement journey started earlier than he wished. He lost his home, retirement savings, and marriage of 23 years at the age of 58. But by 61, Grant discovered affiliate marketing and began rehabbing homes for the local bank. He met the love of his life about 10 years ago and they’ve been married for 8 years. He was able to get back on track for retirement at 68.

Retirement Reality

Retirement Awaits: What does a day in retirement look like for you?

Grant: Get up, have my coffee while doing my social media tasks for the day, making posts, and answering emails. Then, I write content for 2–3 hours. Sometimes, I take a 2-mile walk (if it’s not gym day). By noon, I’m ready for lunch and then whatever recreation is planned for the day, usually golf. I end the day with dinner, spending quality time with my wife, and then work on more content for 2–3 hours.

Your Retirement Plan

Retirement Awaits: Did you have a solid plan going into retirement?

Grant: I did originally, through rental properties, that were going to be my retirement income, until I lost it all. I had to regroup. My only plan was my daily task plan for my affiliate marketing business that I needed to accomplish each day to reach my goals.

Best Part About Retirement

Retirement Awaits: What’s the best part about retirement?

Grant: My time is mine (and my wife’s), regardless of what I’m doing.

Challenges In Retirement

Retirement Awaits: What’s the biggest challenge in retirement?

Grant: At this point, keeping a handle on the budget.

Cost Of Retirement

Retirement Awaits: We want people to understand how much retirement really costs. How do you manage your money now? Do you have a budget, meet with your advisor on a regular basis, etc?

Grant: We’re a simple couple. We made a list of all the cash out and cash in, planned our budget, along with goals to improve the cash in, and monitor and reflect on it weekly.

Retirement Advice

Retirement Awaits: What’s the best piece of advice you’d give someone about to retire?

Grant: Don’t put it off because you’re afraid. You’ll never be ready in your own mind. There will always be doubts and what-ifs. And then, before you know it, you’ll be too old to enjoy anything.

Things I Wish I Would Have Known

Retirement Awaits: What are a few things you wish someone would have told you about retirement/this season of life/transition?

Grant: I was self-employed pretty much my entire life and never really started even thinking about retirement financially until my late 40s. I wish someone had told me to get with an advisor early on and had a set financial plan that would have made it a lot easier and less stressful.

Best Retirement Vacation

Retirement Awaits: What is your favorite vacation or vacation spot?

Grant: We enjoy Fort Walton Beach, Florida, in colder months and Gatlinburg, Tennessee, in the warmer months.

If you want to learn more about Grant in retirement, visit his Facebook page, YouTube Channel, or website.

And for more retirement inspiration, check out other diaries:

[ad_2]

Source link

For many Americans, the importance of planning for retirement has in recent years become an essential financial priority as many soon-to-be retirees are gearing up to exit the workforce in the coming years.

As people get older, retirement planning takes a superior position among other financial priorities. In a time where the cost of living is constantly rising, against the backdrop of an uncertain future, planning for your financial future becomes increasingly challenging as you start to age.

The state of retirement in America

In recent years, several studies and surveys have found that it’s become increasingly hard for Americans to save and boost their retirement savings due to ongoing economic risks

In a GOBankingRates survey of 1,000 Americans aged 18 years and older, around 32.9% had no more than $100 in their savings account. A similar study published in 2022 found that nearly 22% of Americans had less than $100 in their savings accounts.

There’s no correct time or age to start planning or saving for the future, especially when everything seems to have so many added risks these days.

According to a Northwestern Mutual 2021 Planning & Progress Study, Americans have in recent years been increasing their retirement savings, with the average retirement savings account growing by 13% from $87,500 to $98,800.

Despite many bumping up their saving efforts, soon-to-be retirees, those aged 55 to 64 have a median savings balance of $120,000, while younger U.S. adults, under 35 currently have a median account balance of $12,300 according to a PwC report.

A number of unplanned scenarios throughout the last few years have forced many people into early retirement. Those who were unable to properly save and plan, have in recent years stepped out of retirement and back into the workforce as a way to financially sustain themselves.

The average age of retirement has increased from 60 in 1990 to 66 in 2021 and with the majority of adults now living longer than previously, enjoying life after work can be costly if you don’t start planning well before the age of retirement arrives.

Retirement calculation – cutting costs before retirement

Economic uncertainty and rising costs have beckoned American adults to start saving early on in their careers.

From this, research shows that for younger earners, those born between 1981 and 1985, the retirement outlook is more optimistic, as experts predict them to have the highest inflation-adjusted median annual income by the time they reach 70.

Early millennials, as they’re called, will see a 22% increase in their annual earnings once they enter retirement, compared to pre-boomers, or those workers born between 1941 and 1945.

Generation Z, individuals aged 19 to 25 are even better at saving for their future, with a majority of them putting away on average 14% of their income according to one BlackRock study published last year.

Younger generations have more confidence, and more optimism when it comes to planning for their retirement and future. Now with a majority of them taking up space in the workforce, financial priorities will soon begin to change, as many look to build a nest egg that could last them through retirement.

Following a strict budget, cutting unnecessary expenses, and learning how to work with money are some of the few things many people are doing to reduce costs to stuff their retirement savings.

Reduce high-interest debt

Inflationary pressure throughout much of last year has seen an increasingly high number of American adults lean on credit cards and personal loans to help them pay for everyday expenses. As of 2023, close to half – 46% – of U.S. adults carry month-to-month debt, whether it’s credit cards or other interest-related debt.

Keeping expenses to a minimum can start by reducing high-interest debt such as credit cards or personal loans. For the majority of the working class, while it’s still possible to afford it, it’s suggested to minimize any interest debt you may still have, while you’re still receiving a monthly income.

Having this financial safety net means you’re in a position to lower your future expenses and direct more cash towards more important financial goals such as saving for retirement.

Taking control of your debt can be a challenge, as these expenses tend to accumulate over time, so it’s best advised to look at which payments can be dealt with first and foremost, and whether it’s possible to shorten the payment period so that it doesn’t stretch into your retirement years.

Assess your insurance coverage

Another way to cut expenses early on in your career is to assess your insurance coverage. As you become older, health insurance coverage becomes an increasingly important product that you will need to carry for much of your golden years.

Taking the necessary steps now to ensure you have the right insurance coverage will help you better understand what type of product you should take out, and what you are paying for.

Often people only take out insurance coverage later in their life, once they are in a comfortable financial position. While this would make sense at the time, insurance products tend to become more expensive as you age.

While the difference in products may be a few dollars each month, over the long term these quickly add up. Speaking to a financial professional or broker will give you better guidance on which insurance products are best for someone in your position, and will give you the most benefits once you step into retirement.

Take control of student loans

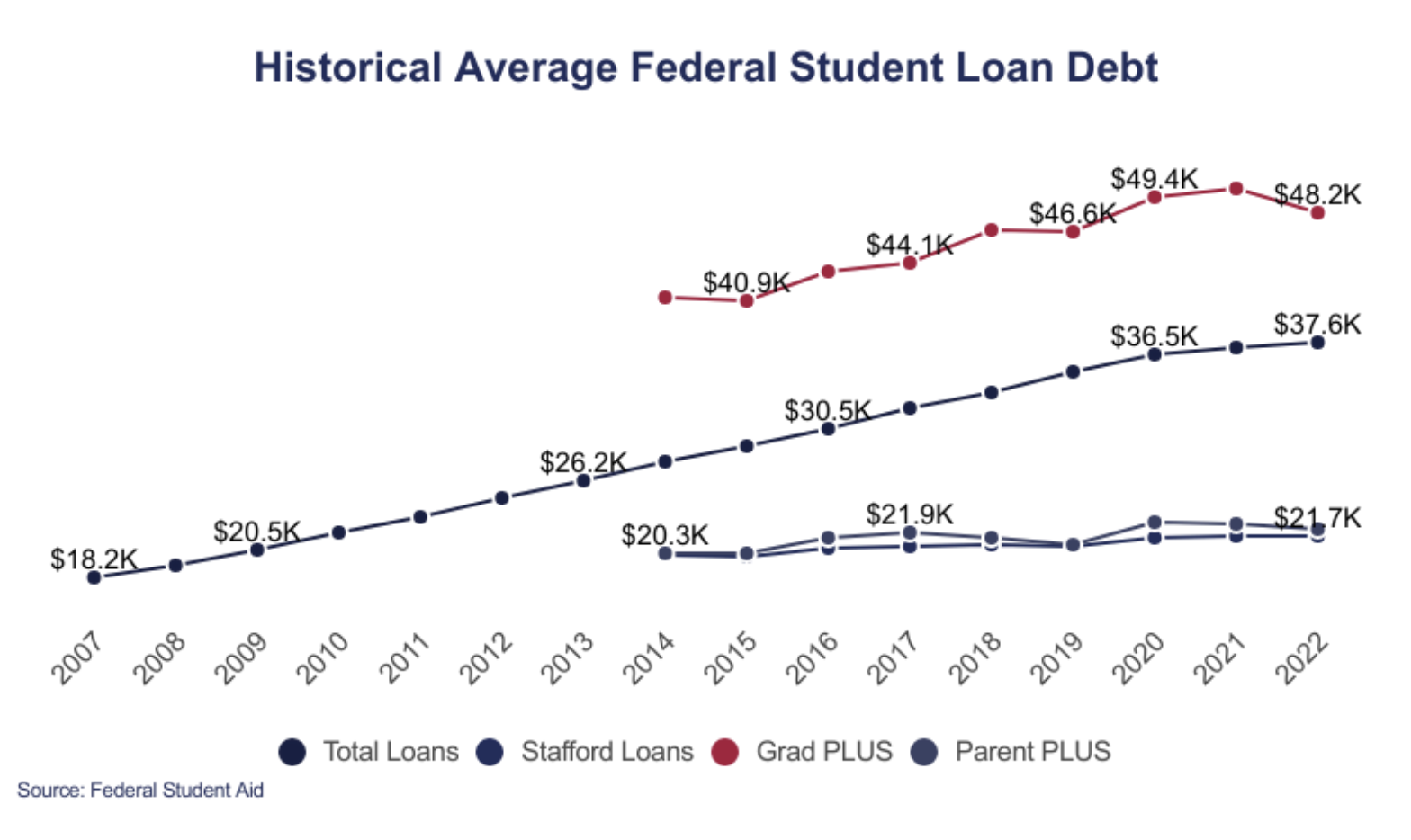

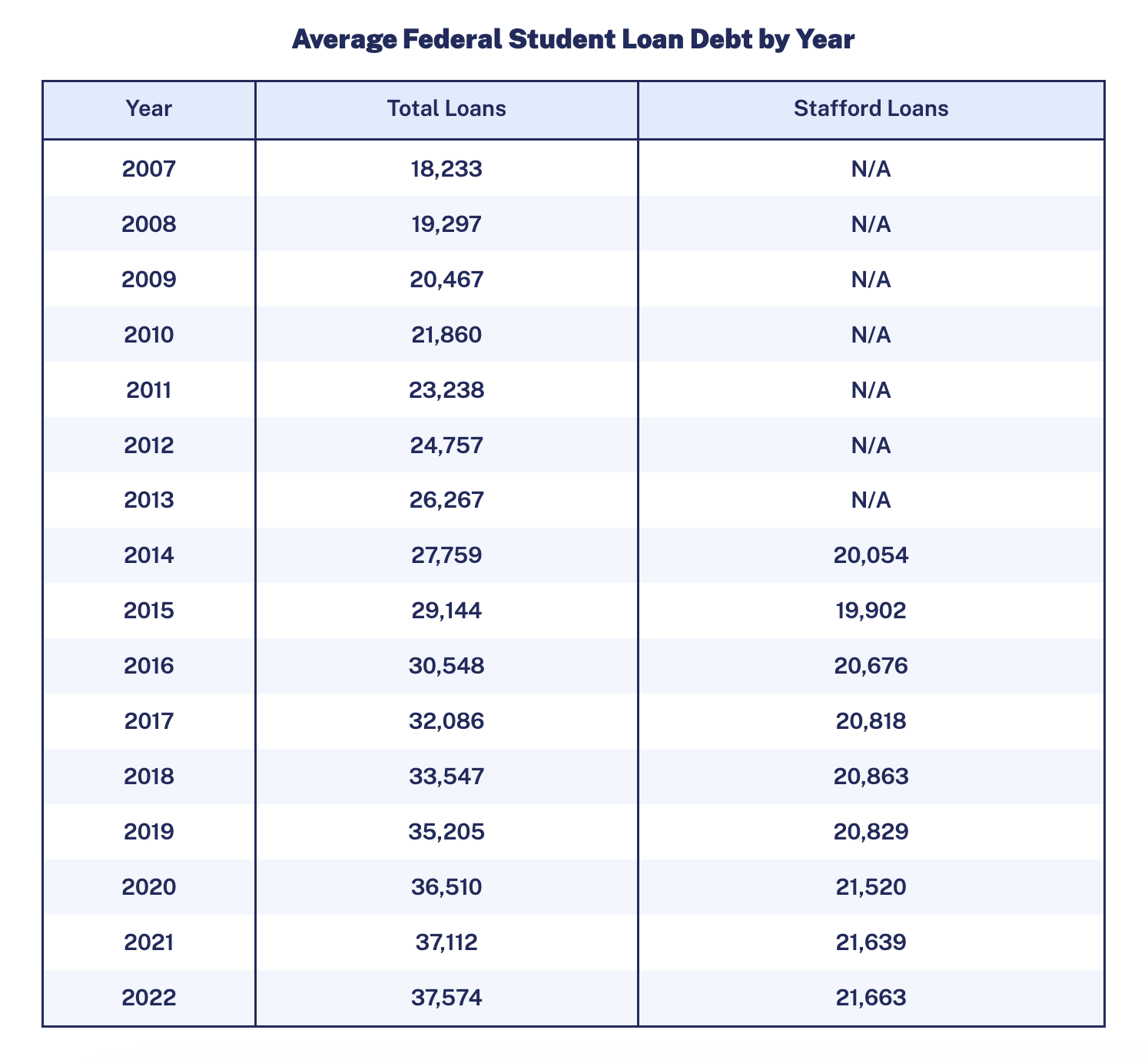

Student loan debt is a massive burden for the majority of American adults. According to the Education Data Initiative, the average federal student loan debt is $36,575 per borrower, while private student loan debt averages $54,921 per borrower.

As of the start of this year, around 45.3 million adults in America have some form of student loan debt, with a majority of them – 92% – having federal student loan debt.

Carrying this debt into retirement is not only a financial burden, but it takes a strain on your retirement savings plans if you don’t manage to prioritize these payments.

Taking more ownership of your student loan debt now will help you in the long term, allowing you to direct more of your financial efforts later in your life toward setting up your nest egg. If you’re not sure how to manage your student loans or have been struggling to make payments, reach out to a financial advisor for guidance, or apply for student loan relief assistance.

If you currently work in the public sector, or for a government entity, see whether there are any student loan relief programs you can qualify for to help lighten the burden.

Pay-off your mortgage

Mortgage rates have nearly doubled in a year, as the Federal Reserve continues with its aggressive monetary tightening, making it more expensive for consumers to borrow money.

In mid-January 2023, the benchmark 30-year mortgage rate was 6.48%, up from 3.22% at the same time a year ago. According to the U.S. Census Bureau, the median monthly mortgage payment sits around $1,100.

Americans have witnessed house prices soar in recent months, as demand grows, supply decreases, and the cost of labor and building materials continue to rise.

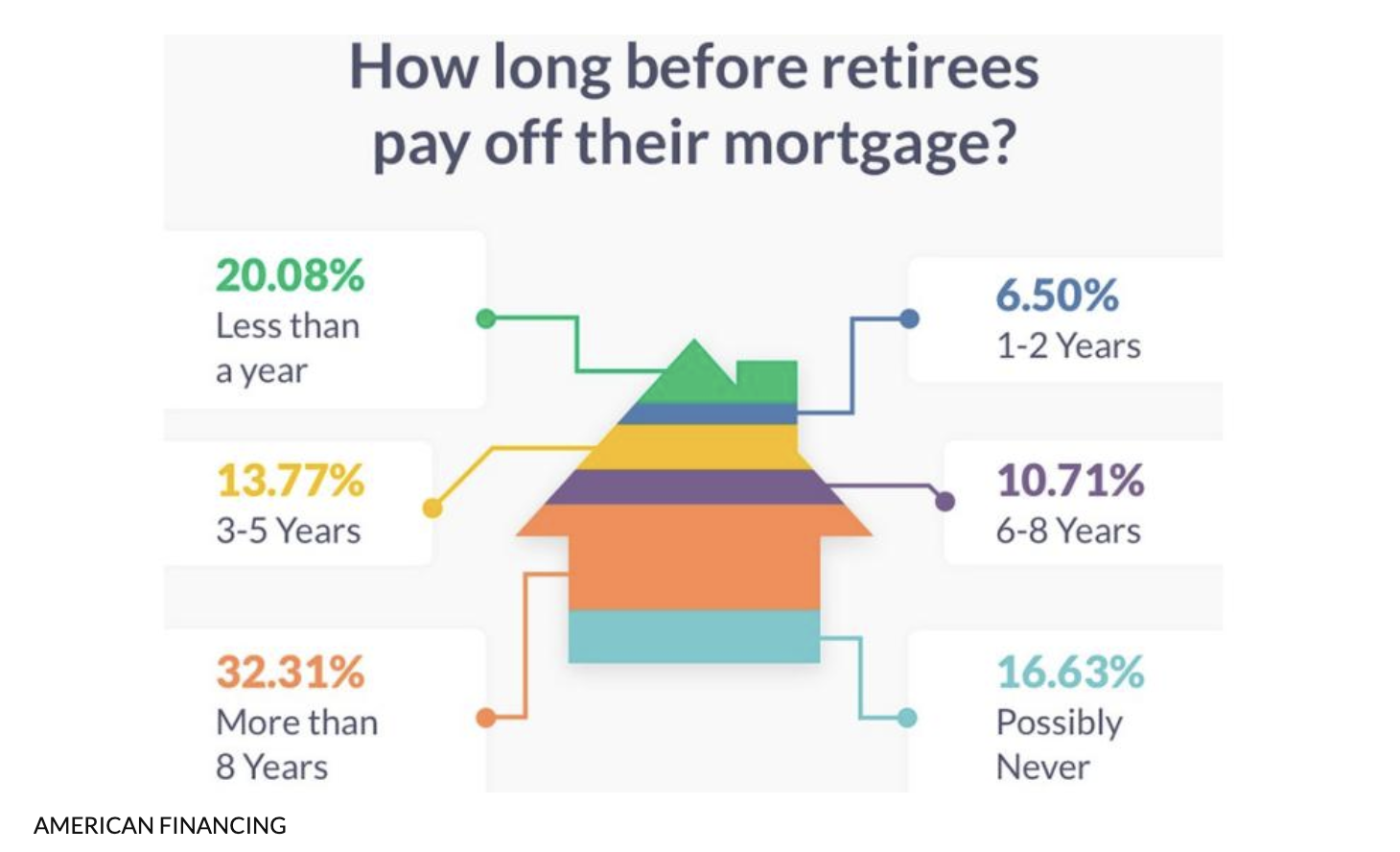

Despite these challenges, many adults still sit with a mortgage by the time they retire. Shockingly enough, 44% of Americans aged 60 to 70 have a mortgage once they step into retirement, with 17% saying they will never be able to completely pay it off according to the American Association for Retired People.

Many soon-to-be retirees and even those still active in the workforce are living with the high cost-burden of their mortgage. Being proactive to reduce these settlements while you’re still pulling a paycheck each month may help you lower your down payment term, but also give you some breathing room to rather put this money towards your retirement fund.

Several different financial programs exist to help homeowners with fulfilling their mortgage payment duties, and often banks provide clear and more concise financial guidance. Take the opportunity to resolve these payments sooner rather than later, and take advantage of lower rates where possible.

Reassess your car insurance

Vehicle insurance tends to increase over the years, and insurance providers adjust payments based on inflation and the market value of your vehicle.

Over time, you may end up paying slightly more for your car insurance, even if you still have the same car, or perhaps have downsized. Values for car insurance are calculated by your insurance provider using the actual cash value (ACV) of your car, to determine how much they will need to pay out in the event of an accident or to conduct any repairs on the vehicle.

What some insurers have done in more recent times, is to provide lower premiums for older customers, to help lighten the expense burdens they might have on their cars. This would make it a lot cheaper and perhaps more affordable for some retirees or car owners to hold onto more than one car.

Additionally, you can approach your current insurance provider to help settle a more manageable insurance premium based on several factors such as years of driving experience, age, and condition of the car, where it’s parked overnight, how often you make use of it, and who the primary driver of the car might be.

These factors, along with others will influence the total monthly amount you will need to pay for your insurance. It’s advised to annually assess your vehicle insurance to make sure you get the most budget-friendly deal available.

Cut unnecessary expenses and subscriptions

Another useful and smart way to minimize your expenses early on in your career is to avoid any unnecessary expenses such as subscriptions, streaming services, and internet bills.

While some may argue that these are essential to their everyday lifestyle and entertainment. The latest figures indicate that the average American spends roughly $114 on video downloads and streaming services, a nearly four-figure increase from 2016.

Internet bills have also increased over the last couple of years, despite seeing a growing number of consumers coming online.