Speculation has grown regarding the possibility of the BRICS countries (Brazil, Russia, India, China, and South Africa) planning to create a centralized currency to replace the US dollar as the world’s reserve currency. While this theory gains traction among critics of the US dollar’s hegemony in the global financial system, experts remain skeptical about the feasibility of such an endeavor.

This article examines the arguments for and against the idea of a BRICS centralized currency and assesses its viability as a contender for the world’s reserve curency.

The Current Dominance of the US Dollar

The US dollar’s role in the global financial system is unparalleled. It serves as the primary reserve currency, accounting for around 90% of foreign exchange transactions. Many international trade, loans, and investments are denominated in US dollars, and numerous countries hold significant portions of their foreign exchange reserves in this currency. This dominance is attributed to factors including the strength of the US economy, the stability of its political system, the liquidity of its financial markets, and its global status as a hub of commerce and innovation.

The Vision of a BRICS Centralized Currency

The notion of the BRICS countries creating a single centralized currency stems from their shared desire to reduce dependence on the US dollar. These nations emphasize the need for a more diversified global financial system to mitigate risks associated with relying on a single currency. However, implementing a centralized currency faces substantial challenges due to the BRICS countries’ diverse political systems, economic structures, and financial regulations. Furthermore, lacking a dominant economy within the group complicates the alignment of interests and establishing trust.

The Improbability of Backing the Currency with Gold

Advocates of a BRICS centralized currency propose backing it with gold to enhance its credibility and stability.

However, several obstacles undermine this idea.

- The US owns approximately twice the amount of gold possessed by all BRICS countries combined, making it difficult for the BRICS nations to challenge the dollar’s dominance with a gold-backed currency.

- Linking a currency to gold necessitates stringent monetary controls, potentially hampering economic growth and development trajectories for BRICS nations.

The Difficulty in Making Unanimous Economic Decisions

Achieving consensus among the BRICS countries in making economic decisions, particularly regarding a centralized currency, appears unlikely due to political and economic disparities. Differences between nations like Russia and China compared to Brazil, India, and South Africa hinder cohesive decision-making. Additionally, concerns arise over the willingness of leaders such as Vladimir Putin and Xi Jinping to compromise on monetary and fiscal policies. Navigating these diverse interests poses significant challenges to realizing a centralized currency project.

The Historical Precedent for Changing the World Reserve Currency

History demonstrates that changing the world’s reserve currency is a gradual process, challenging the notion of rapid transformation. The transition from the British pound to the US dollar spanned nearly three decades and required significant global events such as World War I and subsequent economic upheaval. While contemporary global shifts occur, they might lack the magnitude needed for a new reserve currency, particularly one supported by the diverse BRICS countries, to emerge.

Conclusion

In conclusion, the prospect of the BRICS countries creating a centralized currency to replace the US dollar as the world’s reserve currency is ambitious but improbable. While the desire for a more diverse global financial system is evident, challenges including political, economic, and regulatory differences, alongside the feasibility of establishing a gold-backed currency, stand in the way.

Moreover, historical precedent indicates that transitioning to a new world reserve currency gradually requires significant global upheaval and alignment among participating nations. The entrenched dominance of the US dollar presents formidable obstacles, casting doubt on the BRICS countries’ ability to introduce a viable alternative despite their economic strength and aspirations.

Frequently Asked Questions

Q1: What is the basis of the speculation about the BRICS countries creating a centralized currency?

A1: Recently, there has been speculation that the BRICS countries (Brazil, Russia, India, China, and South Africa) might collaborate to create a centralized currency to replace the US dollar as the world’s reserve currency. This speculation has gained traction among critics of the US dollar’s dominant position in the global financial system.

Q2: Why is the US dollar considered dominant in the global financial system?

A2: The US dollar’s dominance is a result of its pivotal role as the world’s primary reserve currency. It’s involved in approximately 90% of foreign exchange transactions, and many international trade, loans, and investments are denominated in US dollars. Factors contributing to its dominance include the robustness of the US economy, the stability of its political system, the depth of its financial markets, and its status as a global hub of commerce and innovation.

Q3: What motivates the BRICS countries’ interest in a centralized currency?

A3: The BRICS countries are driven by a shared desire to reduce their dependence on the US dollar. They highlight concerns about excessive reliance on a single currency and the potential risks associated with this concentration. They envision a more diversified global financial system that mitigates vulnerabilities tied to the dominance of a single currency.

Q4: What challenges could hinder the creation of a BRICS centralized currency?

A4: The proposition of a centralized currency among the BRICS countries faces several challenges. Their political systems, economic structures, and financial regulations differ significantly. The absence of a dominant economy within the group complicates the alignment of interests and the establishment of trust.

The disparities among nations like Russia and China compared to Brazil, India, and South Africa make unanimous economic decisions challenging.

Q5: How feasible is the idea of backing the currency with gold?

A5: Some proponents suggest backing a BRICS centralized currency with gold to enhance its credibility and stability. However, this arrangement faces obstacles. The US owns significantly more gold than all BRICS countries combined, making it challenging for them to establish a gold-backed currency that could effectively challenge the US dollar’s dominance. Additionally, linking a currency to gold requires strict monetary controls that might not be agreeable to all participating countries and could impede economic growth.

Q6: Could the BRICS countries overcome their differences to make unanimous economic decisions?

A6: Achieving consensus among the BRICS countries for economic decisions, particularly in the context of a centralized currency, seems improbable due to political and economic disparities. The varying interests of nations like Russia and China versus Brazil, India, and South Africa make unanimous decision-making highly unlikely. Navigating these diverse interests and achieving compromises poses significant challenges to implementing a successful centralized currency project.

Q7: Is there a historical precedent for changing the world’s reserve currency?

A7: History shows that changing the world’s reserve currency is a gradual process that requires significant global events and shifts. The transition from the British pound to the US dollar spanned nearly three decades and was catalyzed by events like World War I and subsequent economic upheaval.

While contemporary global economic shifts and power realignments occur, it remains doubtful that these changes would lead to the necessary systemic transformation for a new world reserve currency, especially one backed by the diverse BRICS countries.

Q8: What is the likelihood of a BRICS centralized currency replacing the US dollar as the world’s reserve currency?

A8: In conclusion, the idea of the BRICS countries creating a centralized currency to replace the US dollar as the world’s reserve currency is far-fetched. Challenges stemming from political, economic, and regulatory differences and the difficulty of establishing a gold-backed currency make this idea highly unlikely. Moreover, historical precedent demonstrates that transitioning to a new world reserve currency gradually requires significant global upheaval and alignment among participating nations.

The entrenched dominance of the US dollar further casts doubt on the feasibility of the BRICS countries successfully introducing a viable alternative.

Feature Image Credit: Photo by Jaroline Grabowske; Pexels; Thank you!

The post Is the US Dollar Being Replaced by BRICS?! appeared first on Due.

[ad_2]

Source link

In the past three years, we saw how life could be fleeting and brittle, just like a thread. In the wink of an eye, it may break or shred when we least expect it. Indeed, life is too short to spend on our stressful nine-to-five jobs or risky businesses.

The unprecedented events that have transpired showed nothing was wrong with exploring everything the world has to offer. Leisure travel and experiences are priceless investments in ourselves.

But let’s face it. What will happen when we can’t make a living or find a secure income stream anymore? What will happen to us when we enter our golden years? As repetitive and monotonous as it may sound, we must plan for our future. We already know it for sure. Yet, we don’t know precisely how to achieve our financial investing goals.

With the current macroeconomic conditions, we must have substantial money in our retirement or investment account to ensure a comfortable retirement life down the road. It allows us to be financially secure or independent without a job or a business. Therefore, we will not have to bother our successors when the time comes.

But that is not the sole upside of retirement planning. Investing in a retirement plan or having non-retirement investments has become more vital than ever. If we do it as early as possible, we can earn more. Our retirement accounts, savings accounts, investment accounts, and brokerage accounts can promise higher income, allowing us to retire early. It will also allow us to reap the returns of our retirement and investment strategy while we still have energy.

This article will focus on building and protecting your retirement and non-retirement funds. We will provide tips to increase and diversify your non-retirement investments in your portfolio. Also, we will help you optimize your non-retirement accounts and maximize savings.

Inflation and Retirement in the US

Retirement is almost every employee’s goal. The idea of not dragging yourself out of bed when the alarm goes off is appealing. We will not have to skip breakfasts and queue up while checking our phones to catch the bus or train. Even better, we will not have to work overtime to meet endless deadlines. We will have all the time in the world to do everything we have always wanted. Travel? Reading books all day? Watching our favorite series? Spending more time with families and friends? Put up a business where we will be our own boss? No matter how old we are, we yearn for something we can’t get or do while working.

However, the current macroeconomic indicators are not on our side. Of course, I am optimistic about the improvement in the latter part of 2023. But we must deal with the potential economic slowdown in the first half.

No law prohibits anyone from retiring before they reach the age of 66 or 67. About 50% of employees aged at least 55 have retired from work in the past three years. Also, nearly one in five employees retired before the age of 65. Others aim to retire when they turn 55. but the younger generations wish to retire at 40.

Sadly, the scar of economic crises in 2004-2008 remained evident even after a decade. Many would-be retirees were forced to use their retirement savings accounts to cover household expenses. Likewise, many seniors and retirees had to live in debt. After the crisis, we learned the importance of retirement planning.

The situation has remained bland in the last year while economic forecasts were still bleak. Although unemployment is still a far cry from the labor market scenario in 2009, older adults are still wary. They don’t mind extending their working years to meet their daily expenses or increase their retirement funds. The sharp spike in inflation is one of their motivations.

In a recent study, about half of adult workers are planning to stay out of retirement. In fact, over 30% of workers in their fifties plan to postpone their retirement. Meanwhile, about 20% of workers in their sixties will work longer. With that, the average retirement age in the US is 66 vs. 62 in 2022. Although it’s the same as the legal retirement age, the increase has been noticeable. We must also note that the retirement delay rate has doubled in the last two years.

Moreover, the impact of inflation has already extended to retirement savings. Another recent study shows that 50% of workers paused their retirement savings in 2022. Over 40% stopped putting money into retirement funds like 401 (k). Even more, almost one-third of employees withdrew some of their retirement savings. The cost-of-living hike drove all these. So, it is unsurprising that 72% of the respondents have already reassessed their retirement plans. Among them, 27% reevaluated their financial goals and strategies.

But this year, we may see an improvement as inflation continues to relax. We started 2023 with inflation landing at 6.4%, a 30% drop from the 2022 peak. Indeed, the efforts of policymakers have started to pay off. Meanwhile, the Fed stays conservative as it keeps increasing interest rates. They may peak this year, but increments may slow down while inflation decreases. The impact may materialize in the second half, which can reduce the cost of living in the US. Even better, I don’t think the potential economic slowdown will lead to a deep recession. After all, inflation was more of a demand-pull than a cost-push. As demand softens and supply chain bottlenecks clear up, the market may correct itself and bounce back.

Likewise, retirees are optimistic about the economic conditions in the US. The same study shows that 57% believe the economy will be more robust this year. Also, over 60% expect an improvement in their retirement plans. Recessionary fears are still present, but pessimism is starting to waver. In the long run, macroeconomic indicators may become more stable. Adult workers may have more excess money for retirement funds and non-retirement investments.

Growing Your Funds: The Basics of Retirement vs. Non-Retirement Investments

Many people invest most of their savings and investments in individual retirement accounts. Yes, maximizing their potential in growing your retirement funds is essential. Even so, you may look at other efficient options if you have extra income to invest.

For many, maxing out their annual contribution limits on traditional IRA or Roth IRA is enough. But we must find other investments to increase our wealth. These investments, often called non-retirement investments, do not require a special investment account. You will only have to contribute after-tax dollars to these investments. Also, you can access them whenever you want, wherever you are. That is why it is crucial to seek help from a financial advisor to get the right investment advice and strategy.

Luckily, we have different non-retirement investments to choose from. It may be easier for you if you have a background in the financial market. If not, fret not, for we are here to guide you throughout your investment journey. You can find the things you need to learn in this article. But before that, we must first differentiate retirement and non-retirement investments. We will discuss their basics to help you understand better how they work. Here are the two investment choices for you.

Retirement Investment Accounts

Retirement investment accounts are qualified investments due to their qualification for beneficial tax treatments. We can make either pre-tax or after-tax contributions. Also, investment yields are tax-deferred until you make account withdrawals.

They have annual contribution limits and early withdrawal penalties before you turn 59 ½. The typical qualified accounts are 401(k)s, 403(b)s, and other employer-sponsored retirement plans. Individual retirement accounts (IRAs)s are part of qualified investments. They also have annual contribution limits and preferential tax treatment.

Employer-sponsored retirement plans are popular because most employers match employee contributions to a maximum rate. Even more important is the familiarity of older adults with these plans, so they often invest their funds there. These are easier to manage since their contributions are automatically deducted from their paycheck. As such, convenience becomes inertia in investing.

Non-Retirement Investment Accounts

Non-retirement investments allow you to invest without investing in a tax-advantaged retirement account. You can access this type of investment anytime and anywhere. You can have numerous goals when opening an account. For instance, you can invest to increase your retirement wealth or grow your extra dollars for future use. Put simply, non-retirement investment accounts are investments aside from defined benefit and retirement plans.

This investment type can be anything from the same stocks you hold in your 401(k) to purchasing properties or investing in a private or publicly-traded business. Again, the goal is to increase wealth matching your need for capital. Of course, it comes at a greater risk due to higher reward potential than just saving money for retirement.

Moreover, non-retirement investments are non-qualified accounts, meaning you invest using after-tax dollars. Unlike employer-sponsored retirement plans, one benefit of non-retirement investments is your control over them. You are free to choose whatever investments are available in the market. It also allows you to make your own investment strategy since it doesn’t have rules and limits. You can withdraw or sell it, but yields are subject to capital gains tax.

But before venturing into non-retirement investments, you must ensure financial security. You may start by determining whether you have adequate money in your retirement account. Do you have enough funds in your retirement accounts for your retirement goals? Do you have emergency funds that will last for three to six months? What are your risk tolerance and financial goals? Doing so will help you become more organized and strategic in handling, increasing, and protecting your assets.

You must also consider investment fees, especially when opening a brokerage account. You may go solo, but letting an expert do everything on your behalf will also be helpful. Also, your risk tolerance will dictate the volatility you can tolerate. Meanwhile, your time horizon will reveal your investment preference. It works hand-in-hand with risk tolerance since financial goals in the short run are suitable for less volatile investments like bonds and time deposits.

Things To Do When Investing Your Non-Retirement Funds

A lot of non-retirement investment advice includes complex formulas and strategies. But sometimes, you only need to pause and look at the bigger picture before deciding. Non-qualified or non-retirement investments promise more returns, but risks are higher. These are the essential things to remember to make your investment journey easier and more efficient.

Check retirement investment options

There are various tax-advantaged and taxable accounts for retirement investments. While you can access it in a bank and other financial intermediaries, your employers may be better. Traditional IRAs, 401(k) plans, defined benefit plans, and Roth IRAs are typical options. But know that you can only invest in the available options per account.

Maximize the advantages of retirement funds

Before investing your non-retirement funds, you must max out all your retirement funds. With the volatile economy and recession fears, it is crucial to maximizing the advantages of retirement plans like 401 (k)s. For instance, if you avail of a plan from your company, it will match your contributions at a certain limit. Basically, that’s free money in a secure and risk-free account. Also, Roth IRAs earn tax-free until you withdraw them.

Start early, earn exponentially

The early bird, indeed, catches the worm. If you start saving and investing early, you have more time to study your investment options and grow your funds. You also have better flexibility to market volatility since you are more familiar with the market trend. As such, you can cope with it through prudent portfolio diversification in technology stocks, bonds, and funds. Aside from that, there are better reasons why saving and investing early can be helpful.

- You will have more time to optimize the potential of compounding interest. You have more time to generate and reinvest investment yields in other accounts. For instance, you invest $5,000 with a compounding interest of 5% yearly. If you invest at 25 and retire at 66, the future value will be $36,959. But if you don’t invest until you’re 45, you will only have $13,930.

- You will be more disciplined, making saving and investing a lifetime habit.

- You will have more time to cope and bounce back from investment losses. With that, you can also try other investments, especially those with high risk and reward potential.

- More years to save means more money upon retirement.

- More experience in investing means expertise in various investment types. It will allow you to go solo and avoid brokerage fees.

Assess your assets and liabilities

In the world of investing, you must spend money first before you earn more money. So before you invest, you must assess your financial capacity to do so. You can start by assessing your net worth, the difference between assets and liabilities.

Your assets include cash and cash equivalents, such as cash on hand, cash in banks, and short-term investments. Other assets are in the form of real properties like houses and personal properties like jewelry. Meanwhile, liabilities include car loans, mortgages, student loans, medical expenses, and unpaid household bills.

Once you list all assets and liabilities, subtract the total liabilities from your total assets. The net value will be your net worth. Then, you can add your net worth to your retirement goals. You can check your net worth from time to time to see if it is in line with your goals. A negative net worth means you have excessive liabilities and no room for more risks. From there, you can find ways to improve your finances before starting your investment plan. Remember that liquidity is king, so you must manage your cash well to increase and protect your wealth.

Manage your emotions well

Crests and troughs are constant in the world of investing. One of the first things to learn is to manage your emotions well. Often, investors are carried away by market sentiments. Bearish views are common during market corrections, so beware.

Typically, an investor may become overconfident when investments perform well. He tends to underestimate market risks, leading to a bad investment decision. Meanwhile, an investor becomes anxious when assets are in a downtrend. He may sell investments instantly, even at a discount, leading to investment losses. Corrections are more common in the stock market. So, investors must be keen during a breakout to avoid bull or bear traps.

As such, it is crucial to avoid becoming an emotional investor. Overconfidence and anxiety may lead to wrong investment decisions. You may lose potential gains or even incur investment losses. Aside from that, you must be realistic with your investments. Observe the actual price and financial trend instead of solely relying on market sentiments. Reading expert analyses and reviews may help, but it’s more important for you or your broker to understand the investment. Also, you may rebalance or diversify your portfolio to make it suitable for whatever market condition.

Consider investment fees

More often than not, your concern revolves around returns and taxes. But exorbitant investment fees may erode the value of your investment. Transaction, brokerage, and administration fees are typical deductions from your funds. You must check them as frequently as you can since fees can offset gains. Calculate the expense ratio to know how much your investments are used for administrative and other expenses. You can divide the fund’s operating expenses by the average dollar value of assets under management (AUM).

Doing so can help you make better investment decisions. That way, you can find more affordable but earning investments. You can choose mutual funds with lower fees or brokers with more reasonable fees.

Suppose you invest $5,000 in a mutual fund with a 2% expense ratio and 5% annualized return. If you withdraw it after 20 years, the gross value will be $13,266. But with the expense ratio, leading to fees of $4,236, you will only get $9,030. But in a fund with an expense ratio of 1%, fees will only be $2,311. The net value will be $10,956. That’s a $1,936 difference.

Avail of insurance or annuities

In general, investments are good. But there’s an unspoken rule to follow when managing your assets. Again, liquidity is king, so always prioritize having enough cash reserves. Once you have enough savings and emergency funds, you may set aside a portion of your income for investments. Then, you must ensure your assets are protected. Insurance and annuities can serve as an extra mantle of financial protection. You will not have to sell your investments at a discount or deplete your savings in emergencies. Insurance will come first before your turn to your emergency funds and savings.

Speak to an expert

You may find yourself saying retirement planning or investing is not your thing. That’s inexcusable. Many financial experts are dedicated to helping you plan for your retirement and investment. Also, you can watch video tutorials or read helpful articles for free.

Non-Retirement Investments To Consider

At this point, you already know the basics of non-retirement investing. These are the investment options you can consider.

Brokerage Accounts

Brokerage accounts are probably the most typical option for non-retirement investing. These are non-qualified accounts, so funding is done with after-tax dollars. With a brokerage account, you can choose from various investment types, depending on your risk profile. These include stocks, exchange-traded funds (ETFs), bonds, and target-date funds.

Among these, stocks are the optimal option, given their high risk and reward potential. But these may require more experience since investors and brokers have to watch price trends, company financials, and market changes. You must value the stock using different price metrics when doing fundamental analysis. Doing so will help you determine if the stock price reflects the company’s intrinsic value. Meanwhile, if you prefer technical analysis, you must observe stock price changes to know when to sell or buy.

Today, it is easy to open a brokerage account. You can do it online as online brokerages become more prolific and impose lower fees. But you have to be more careful to avoid a potential scam. Also, you can find brokerages with higher brokerage fees due to their excellent customer service. Always check their fees and match them with their expertise and quality of service.

Property

Buying properties as passive income is a traditional real estate investment method. You can buy and sell properties or buy and lease them out. Yet today, more common investments, such as real estate investment trusts (REITs) and crowd-funded real estate, are available.

However, many analysts are pessimistic about the real estate performance this year. Property sales and prices are cooling down. Despite all these, I disagree with those anticipating a real estate market crash. First, commercial and residential property shortages remain high. The year started with a 4% decrease in property inventories. We can attribute it to builders becoming more cautious since the Great Recession. With the current supply and demand, price changes may remain manageable.

Educational Plan

Educational plans are another non-tax-deductible savings plan account. Funds can be invested with non-taxable earnings. Even better, withdrawals are taxable for education-related expenses, such as tuition fees and books. It will be helpful if you plan to build a family and expect your child to attend college. But remember that non-educational expense-related withdrawals are taxable with a 10% penalty.

Certificate of Deposits

Certificates of deposit (CDs) are like bonds, but banks and credit unions issue them. It is also logical to classify them as time deposits because they have a fixed term and pay periodic interest. They mature after a certain period, often within a year. Since banks often issue them, they are FDIC-insured, which pays interest. Also, like bonds, they have low risks and lower yields, unlike the other investments on the list.

Government Bonds

There are various types of bonds, but those issued by the government yield some interests with manageable risks. Municipal bonds, treasury bonds, and federal bonds are some typical options. Even better, they are more inflation-linked than corporate and mortgage-backed bonds. Note that most bonds do not perform well in a high-inflation environment. Given the nature of government bonds, they still have decent yields amidst inflation. They also have a better hedge against valuation losses. But overall, bonds have low risk and reward potential.

Learn More About Non-Retirement Investing

Having a consistent income stream is crucial for retirement planning. A passive income can help increase and protect your wealth. As such, investing your non-retirement funds can provide more returns in your retirement years. It is more essential today, given the economic volatility. But no matter how promising they can be, you must be careful and familiar with them before venturing. You must have adequate knowledge, capacity, and patience to do so. Thankfully, various types of investments suit your finances and risk preferences. There are also experts to provide all the help you need for sound investment decisions.

The post Things To Remember When Deciding To Invest Your Non-Retirement Funds appeared first on Due.

[ad_2]

Source link

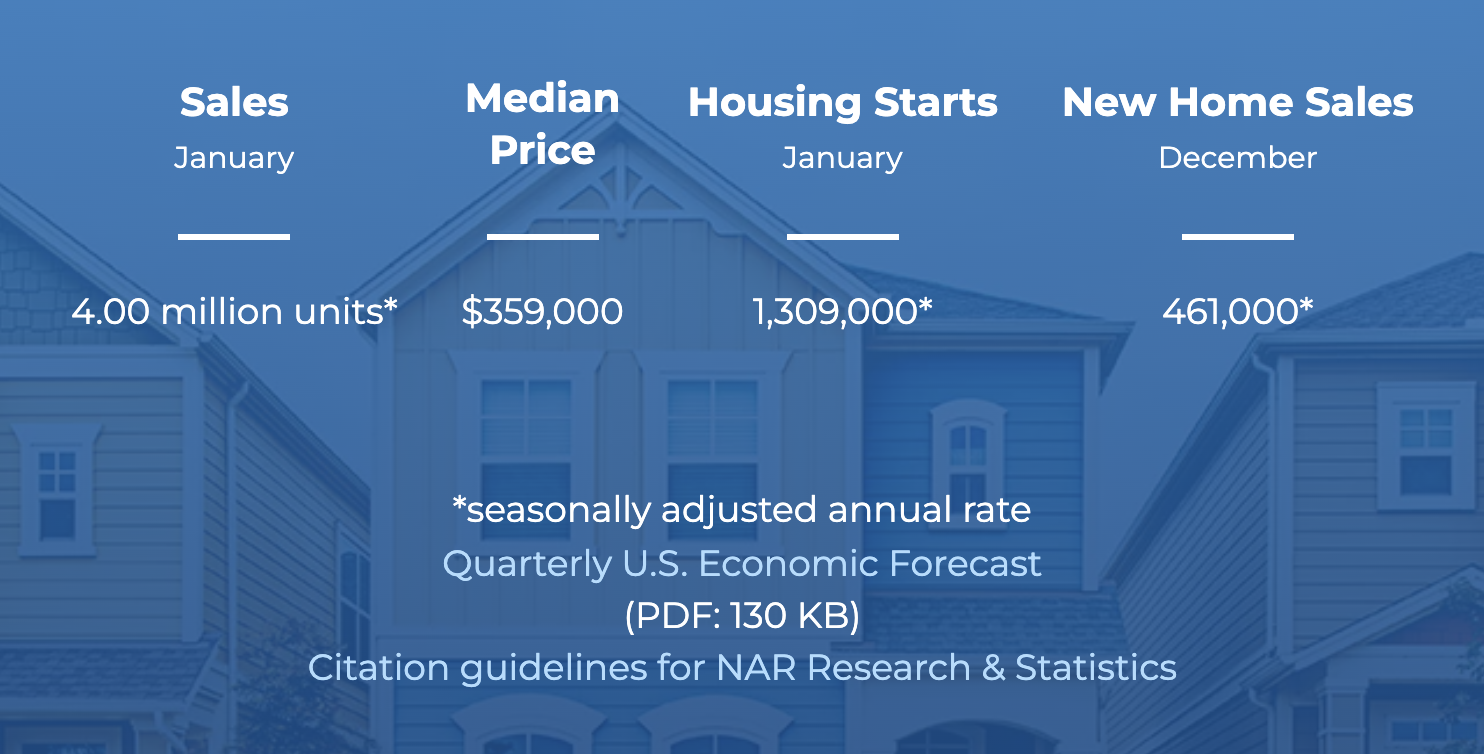

The real estate market is in an interesting state right now. Home sales are slowing because of higher interest rates, but prices in some areas have yet to drop. Overall, the median existing home sales price in January 2023 was up 1.3% from the same time last year, but home prices in expensive areas have gone down, while prices in less expensive areas have gone up.

Considering that home prices were reaching record highs in 2021, one would expect them to have normalized with the slowing market, but that has yet to happen. However, if interest rates continue to rise, prices should continue to drop.

But what does that mean to you and your finances? This article will explore how the current real estate market can impact you financially.

Real Estate Situations that Can Affect Your Finances

There are several situations that you may find yourself in where the real estate market may affect your finances.

1. Buying a Home

If you’re in the market to buy a home, you’re going to pay a higher interest rate than you would have in 2021. However, the inventory of homes is high and the number of buyers is down. That means that you may have more negotiating power with sellers. Prices may be higher, but chances are, most sellers are very motivated which could put you in the driver’s seat.

But you’ll end up paying a higher rate, but with a lower price point for the home, so it may even out for you financially. You can also refinance later if interest rates go down and get ahead of the game.

Be sure to do your research into what is happening in your area in terms of prices and the number of sales that are occurring. Every local market is different. Make sure that your real estate agent talks to you about current comparable sales, and use your negotiating power.

2. Selling a Home

If you’re planning to sell your home in the near future, you may be under a bit of pressure. Buyers are fewer in many areas due to the higher interest rates, so the people that are buying have the negotiating power. If you can, you may be better off waiting to sell until rates go back down. However, what will happen with interest rates and when is a great unknown.

If you need to sell and you want to get a specific profit on what you paid for the home or on what you owe on your mortgage, you can calculate here what price you need to stick to.

Often the best strategy in this kind of market is to price your home higher than what you actually need. That way the buyer can negotiate and feel like they’re getting a deal. It cannot be stressed enough, however, that the best strategy depends on your local market.

Do your homework and talk to your real estate agent about what is happening in your market and what comparable homes are selling for. And if you need to make a certain profit on your home, you can stick to your guns and wait for that buyer that “must have” your home.

Work with your agent to make your home as appealing to buyers as possible by making repairs or upgrades and staging the home well. In a tough market, you need to make your home stand out from the competition.

Also, work with your tax advisor when considering the price that you need to get. Selling at lower price means less in capital gains tax, so that will have an impact on your finances overall.

Special note: there was $400mm in sales in January 2023.

3. Investing in Real Estate

Investing in real estate right now is an interesting proposition. Warren Buffet said “be greedy when others are fearful”. Real estate investors right now are fearful of economic and market instability; however, having that kind of outlook depends on your goals and your risk tolerance.

If you’re looking to flip houses as an investment, it’s likely that you can find deals, particularly on distressed properties. But with the number of home buyers decreasing, you may find yourself having trouble finding a buyer and thus incur carrying costs. You can still make a profit, though, if you can put minimal money into the property and price it competitively based on local real estate conditions.

Your best bet if you want to flip homes now, is to carefully analyze each potential deal, including what is happening in the specific area the property is in, and cherry pick only the deals that make the most sense and have the least risk. With so many “fearful” investors, you’ll have less competition, so you can afford to be choosy.

If you’re considering buying rental properties, it’s still a matter of looking at each deal. The higher interest rates mean that fewer buyers are buying and are renting instead, which can drive rents up. That’s great if you can find a great deal and pay cash for the property. If you need to finance the property, however, you’ll be paying a higher interest rate which will reduce your cash flow.

The bottom line is, if you’re considering investing, you have to really understand your local market. Do considerable research before making a decision.

5. Refinancing Your Mortgage

Clearly, if your current interest rate is lower than current mortgage rates, refinancing your mortgage may not be a good idea, and vice versa. You also have to consider your closing costs when deciding if refinancing is financially beneficial.

If you are refinancing to a lower rate and getting cash out from your equity, you may find that when the bank assesses your home’s market value, it may be lower than you think. Again, it depends on what’s happening to prices in your local market.

If you want to refinance to a shorter loan term, you may still be able to benefit. Rates on 10 or 15 year mortgages are generally lower than 30 year mortgages, but your payment may still be higher because of the shorter term.

Another thing to consider is that lenders tend to be more conservative in a slow real estate market, so it may be more difficult to qualify for the refinance. Credit score and income requirements will be tighter, so be prepared to go through a more rigorous application process.

Your best bet is to shop around for the best rates and terms, analyze your options, and decide which option, if any, is right for you.

Here is a nifty refinance mortgage calculator to help you.

6. Home Equity Loans

If you’re considering getting a home equity loan, whether the real estate market will impact you depends on your goals.

If you want a home equity loan to consolidate other debt, current mortgage rates are still likely lower than the rates on other debt such as credit cards. However, similar to a cash-out refinance, your equity may not be as high as you expect based on market values.

If you want a home equity loan to remodel your home, if you’re doing it just because you want your house to be nice and you can afford the payments, go for it. You might want to consider a home equity line of credit with a variable rate so that the rate goes down when rates go down in general. However, rates may also go up.

If you want a home equity loan for remodeling, but with the goal of selling your home for a higher price in the near future, you’ll need to give it careful consideration. If rates continue to rise and home prices fall, you may not get your money back from the remodeling you do and the interest you pay on the loan. Be sure not to overdo your improvements.

7. Renting

Fewer people buying homes means more people renting, which is creating a rental shortage due to high demand. As a result, in 2023 many predict that rental price growth is likely to remain high, which is bad news for renters.

Other economic factors are also decreasing the amount of income that renters can spend on rent. What this means is that rentals in higher-priced areas will be less in demand, which should start to force prices on those rentals down a bit.

In the longer term, rental prices are likely to start to come back down, so if you’re finding it difficult to afford current rents, you may only be struggling temporarily.

As with all the other effects of the real estate market, how the current conditions will affect renters is location dependent. If you’re in the market for a new rental, do your homework and shop around, and don’t be afraid to negotiate with landlords to try to get a better rate.

In Closing

The real estate market is interesting right now, and it’s difficult even for experts to predict exactly what will happen in 2023 and beyond. Many factors will have an impact on the market’s direction, so you should stay informed about what’s happening in the market, particularly in your area.

If you’re in any of the situations discussed, be sure to do your market research and look to professionals, whether it be a real estate agent or a financial advisor, for advice. By doing so, you can find ways to successfully navigate this unpredictable market and protect your finances.

The post How the Current Real Estate Market Can Affect Your Finances appeared first on Due.

[ad_2]

Source link

You are probably concerned about your bank account balances these days. This is especially true if you are living paycheck to paycheck — which according to a 2022 Lending Club report is approximately two-thirds of the population. To make matters worse, your anxiety is likely heightened by inflation and the prospect of a recession.

However, there are a few basic things you can do to lower your financial stress, as well as your budget:

All seem relatively easy. What’s more, it doesn’t take a lot of money to lower your financial stress. The exception, of course, is starting a side business. According to the U.S. Small Business Administration, the average cost to start a microbusiness is $3,000, while the average cost to open a home-based franchise is $2,000 to $5,000.

However, what if you could earn money from home without spending a dime? It may sound too good to be true. But, here are 20 real ways to make money from home for free.

1. Sell your skills on Fiverr.

Even if you have a full-time job, using Fiverr, you can monetize your time and specialty skills. Basically, it’s a website where you can find micro-jobs. The purpose of such services is to facilitate the quick completion of standalone tasks for an individual, business, or employer. Depending on the task, you can earn $5 and up. Over time, though, there’s potential to earn several hundred dollars per month.

There is a wide range of tasks that can be performed, including writing letters, answering emails, performing minor graphic functions, and anything else that is similar. But, don’t let your intimidation get the better of you. The platform lets you choose which skills to offer.

As you browse Fiverr, you’ll find a lot of ideas to help you get started, as there are many success stories. Plus, this is an absolutely free way to earn money online without investing anything.

2. Work as a virtual assistant.

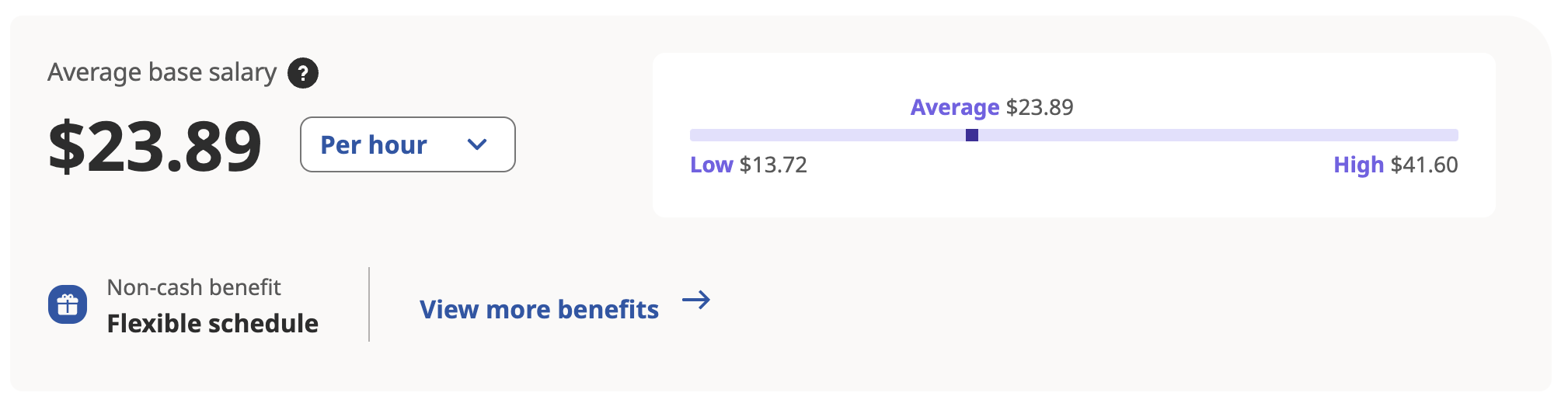

Are you good at organizing and planning? If so, becoming a virtual assistant can be an excellent way to earn extra income online. As a virtual assistant, you manage social media pages, respond to emails, and take phone calls for businesses.

In response to the increasing number of solopreneurs, virtual assistants are experiencing an increase in demand. Getting started is as simple as applying for jobs on Upwork, Indeed, or Virtual Assistant Jobs. According to Indeed.com, VAs earn an average of $23.89 per hour.

Virtual assistants have also found success by building their own personal brands and promoting them to entrepreneurs. Consider creating a Facebook Business page and filling it with content that promotes your business. Don’t worry. You can create one for free and share it anywhere online.

3. Become a JustAnswer expert.

For subscribers, it costs $74 per month to access unlimited expert answers with JustAnswer. Providing timely advice, the site seeks out experts such as veterinarians, mechanics, home repair specialists, and lawyers.

As such, it can be a sweet gig if you have expert knowledge. It’s simple. You answer questions and earn money helping others. In addition to talking, texting, and chatting, you can send documents and photos that might help solve the problem.

When you become a new expert, you’ll earn 20% of the user’s payment. It is possible to work your way up to 50% of the fee with enough consistently high ratings over time. The payouts are made through PayPal.

As well as the aforementioned expertise, you can also provide assistance with appraisals, pets, and teaching. In other words, there are many subcategories that make it accessible to individuals with varying levels of experience.

4. Write on Medium.

Experts and undiscovered writers can share their writing on any topic on Medium. You can use Medium instead of starting a blog from scratch. With Medium, you can begin earning money right away, as opposed to purchasing a domain and web hosting.

Also, using Medium as a platform for writing can be an excellent choice if you don’t want to spend months or years writing on a blog without making any money. Writers on Medium get paid for their stories based on how many people read them and interact with them.

Most writers on the platform make less than $100 per month, but the top earners make more than $10,000 per month. The best way to become a top earner is to post a daily article for a long period of time. Your earnings will increase as you write more articles and as they become more popular.

Another advantage of Medium? Instead of picking a niche straight away, you can develop your voice gradually. You might start writing on Medium and then start a blog once you find your sweet spot of readers’ interests and your own interests. The same content could be used for your blog and Medium site, but be careful not to ruin your search engine optimization. Whenever possible, post your writing to your blog first, followed by a Medium post, referencing the original post.

5. Join a focus group.

Do you enjoy expressing your thoughts and opinions? If yes, then why not participate in paid market research studies?

The purpose of focus groups is usually to determine the attitudes of people toward specific products, brands, or ideas. It may also be possible to ask participants about their opinions on competitors’ products or services. It depends on the focus group, but you can expect to get a salary of $30 to $150 for an hour for a focus group — although some very specific focus groups pay up to $450 for an hour.

Participants in focus groups are usually paid handsomely, and they can be held in person or online. There are several places where you can find focus groups, including:

- User Interviews

- Respondent

- FocusGroup.com

- L&E Research

- 20 | 20 panel

In most groups, there will be a moderator who guides discussion, takes notes, and records the meeting. You can participate in an online focus group using video software on your smartphone, tablet, or computer if you join one.

6. Review a mock trial.

Are you a fan of court procedurals? Is “The Lincoln Lawyer” and other John Grisham adaptations your cup of tea? Online mock trials might be a good fit for you if so.

Websites such as Ejury.com, OnlineVerdict, and Virtual Jury pay you for watching a mock trial from the comfort of your own home. In return, jurors will receive payment amounts ($20-$60) based on the amount of time it takes to review a case.

7. Become an online researcher.

Do you have solid Google skills? If you are able to provide reliable sources and information for companies in a variety of fields, you may be paid. You can now earn a paycheck for doing web deep dives.

Examples of companies that hire online researchers on a regular basis are:

- 10EQS

- Boston Scientific

- Chainlink Labs

- CrowdStrike

- Edmentum

- Humana

- Parexel

- Robert Half International

- Twilio

- Wonder

Applicants may be required to have a bachelor’s degree and research experience by some companies. As for the pay, it can range from $8 to $35 per question answered.

8. Take online surveys.

There are a lot of ways to make money online, but this is probably the most common. It is possible to participate in popular online survey platforms, such as:

- OneOpinion

- Survey Junkie

- Inbox Dollars

- Swagbucks

- Ipsos iSay

- Opinion Outpost

Monthly earnings range from a few dollars to several hundred dollars. Additionally to earning cash, some survey services offer points that can be redeemed for prizes or gifts.

Prior to participating on any platform, be sure to do your research. There are a lot of scams in this field, unfortunately.

9. Enter data entry.

Making extra income through data entry has long been a popular side job for people. In the past, these positions were temporary within a company. However, online work-from-home opportunities have transformed the potential of data entry. Even better, the job requires very little training, so it’s a great choice.

Input or uploading information can be done using a keyboard, scanner, or other devices that allows input or uploading. Because payment is usually based on your words per minute (WPM), you’ll need to learn to type quickly.

Freelance job sites like Upwork are the best place to find data entry jobs. Companies that outsource these jobs can be found on these sites. Still, there are temporary agencies that offer these same office jobs online. If you are looking for data input, data entry specialists, or data entry operators, consider job sites such as Monster and Indeed.

Salary.com estimates that the average hourly wage for a Data Entry Clerk I in the United States will be $17 on January 26, 2023, but the range will typically be between $16 and $20. Also, be sure to stick with reputable job marketplaces and agencies, as this type of job is prone to scams.

10. Transcribe audio and video files.

Speech-to-text transcription is getting easier with artificial intelligence, but it’s still not perfect. As a result, a large number of companies use transcriptionists to turn audio from videos into text that is accurate.

With companies like Rev, you can work part-time or freelance on specific projects with various firms. You are usually able to choose which assignments you want to work on and set your own schedule at most companies. In addition, no money is needed upfront — just use the computer’s speakers to transcribe.

You’ll need strong typing skills to succeed as a transcriber. Also, for clients to understand your work, it must be error-free and easy to understand. You can practice transcribing short audio files so that you’re ready to apply for transcription jobs.

When transcriptionists are just starting out without a specialization or expertise, they usually make between $15 and $25 an hour.

11. Launch a YouTube channel.

Have you ever considered becoming a YouTuber? With today’s smartphones, you can make funny skits, unboxing videos, and product tutorials. Also, you can set up your YouTube channel for free. You can create a YouTube channel with your name or a custom name by signing into your Google account.

It is possible to earn money as a YouTube channel owner in several ways. When your channel reaches 1,000 subscribers, you can start earning money with ads. Your YouTube channel can also be monetized by partnering with brands, selling merchandise, or becoming an affiliate.

You need to focus on one niche if you want your YouTube channel to be successful. Whether you want to offer beauty tutorials, reviewing tech products, or summarize cryptocurrency prices every day, you can do whatever you think will attract more viewers.

12. Sell your used items.

Are there items in your home that are collecting dust and taking up space? Wouldn’t it be great if you could sell them online and make a profit?

eBay is one of the most famous sites for selling everything from books, collectibles, and cars to clothes, art, and furniture. You can choose from multiple categories and sale options, including an auction and a “Buy It Now” option. Make sure you know what things are selling for, describe your content clearly, and offer several visuals to attract attention.

Craigslist is another popular marketplace for used goods. You can list items for free on the site for others in your local area to see and possibly purchase. In recent years, numerous apps have emerged that have become immensely popular for quick sales, such as OfferUp. Unlike many of eBay’s sales, these are primarily for local pickups rather than shipping.

Through Facebook Marketplace, you can also sell socially. It is also regarded as an online and local sales process, so plan on meeting up with buyers for the delivery of items.

Furthermore, other online sites work well for specific niches that you may want to target. Poshmark, for instance, offers gently used designer clothing and accessories, along with some branded home goods. When it comes to tech equipment, DeCluttr is an ideal solution for getting rid of older smartphones, tablets, and more. Additionally, video games, CDs, and DVDs will be accepted.

13. Take photos and sell them online.

If you have a good collection of photographs, you can sell them as stock images to companies. You will earn a small commission every time someone downloads your image from the company. These are a few examples of websites where your photos can be sold:

- 500px

- Alamy

- Adobe Stock

- Burst

- iStock

- Shutterstock

- Stocksy

- Zenfolio

Another option? Sign up for a print-on-demand marketplace like Printful, Redbubble, or CafePress to sell your photography prints online. Using these platforms, you can upload images and sell physical products while they handle inventory, printing, packaging, and shipping for you.

14. Become a social media consultant.

A social media presence is a must for any business, but just having it doesn’t mean companies know how to manage their accounts effectively. In a consulting capacity, you could utilize your social media skills to help companies gain followers.

Because your profile serves as your portfolio, it’s pretty simple to promote yourself. You should specifically market your portfolio on digital marketing forums and groups. And, when you reach out to agencies, include a link in your email.

According to ZipRecruiter, the national average for social media consultants is $52,453 per year.

15. Get paid entertaining yourself.

Can you think of anything better than working from home? What about working from home while doing something you enjoy?

- Watching videos. On your mobile device or laptop, you can watch movie previews, TV shows, news, commercials, and more with Swagbucks or Inbox Dollars. You can redeem your points for cash via PayPal or gift cards from different retailers in exchange for points.

- Listening to music. If you’re interested in listening to and rating music, you might want to register with Slicethepie, Playlist Push, and HitPredictor. Each review will result in a payment, but the amounts vary since quality reviews are rewarded. As a result, if you provide a detailed and constructive review, you are more likely to receive a better payout. Payments are made via PayPal to reviewers.

- Playing games. Getting paid for playing games might be fun for gamers. Coin Pop, for example, allows you to exchange coins for cash or gift cards. Despite the small payout and time commitment, the rewards add up over time if you play games on the app regularly. You can also play games on sites like Swagbucks for money.

16. Host travelers in your home.

If you have an extra room or are willing to rent out your entire home, Airbnb can be a great passive income source.

Listing your space on Airbnb is not 100% passive or online. It is still your responsibility to make the place tidy for the guests, to answer questions, and to clean up after they leave. It is always possible to outsource these tasks or to use platforms like YourFront Desk.

The bottom line is that if you have the right location and make your listing stand out, you can make six figures renting out space on Airbnb. Be sure to develop a captivating headline, take stunning photos, and describe your property in detail so that your listing will stand out.

17. Become an online travel agent.

Are you known for finding the best vacation packages and flight deals? If so, put these skills to use as a virtual travel agent.

It is the job of travel agents to help people plan their vacations, business trips, and personal travel. To make their trips easier, many individuals rely on travel agents to help them arrange connecting flights, accommodations, sightseeing tours, etc.

To become an online travel agent, you don’t need any special certification. Instead, it takes to research and organization skills to plan a seamless trip for your clients within their budget. It is possible for you to get discounts for your clients by partnering with different companies.

You might also be able to land a home-based travel agent through job boards like FlexJobs and ZipRecruiter. In the United States, the average salary for an Online Travel Agent is $64,067 per year as of February 16, 2023.

18. Start tutoring.

It may not be too difficult to become a tutor if you are an expert at any of the common subjects, including math and science. Wyzant, Chegg, Skooli, and TutorMe, for example, are websites that can assist you with your work.

Online tutoring has become more common than going to students’ homes in recent years. Even non-conventional subjects, such as test preparation and English as a second language, can be taught. In some cases, people may even wish to acquire specific career skills from you.

Honestly. There are so many possibilities here. Additionally, you could earn several hundred dollars a month.

19. Become a professional dog sitter/walker.

Do you love animals? I’ve always thought walking dogs was a relaxing and enjoyable activity. I mean it’s something that I do on a daily basis. Additionally, you can make money walking while getting some exercise.

Earnings are determined by how often you work. To get your business off the ground, offer a discount to your first clients and ask them for referrals. Ideally, you want to lock in regular clients who will need you for weekly walks.

To get started, find local clients by marketing your services on sites like Rover. Or, ask your friends, family, or neighbors. You may be able to earn more income if you offer pet-sitting services. You can then charge an overnight fee for keeping other animals besides dogs.

20. Refer your friends or family.

You can get paid for referring your friends to some businesses, such as credit card companies, banks, and retailers. A referral page is usually displayed after you have made your own purchase and offers you a personal link to share with others. Everyone who clicks your link and buys the service or product will earn you a referral bonus.

There is a wide range of payouts. For instance, Grove Collective offers $10 for a successful referral, while T-Mobile offers $50. With Capital One’s Refer a Friend program, you can earn up to $500 a year. Your referral can earn you a bonus if they’re approved for a Capital One credit card.

FAQs

How can I make money online?

The possibility of making money fast is one of the attractions of making money online. Considering how many people looking to make money online need money now, this isn’t surprising. In this regard, the web presents an endless amount of money-making opportunities.

However, it is important to treat the process as a business if you want to make money quickly online. There is very little chance of making a quick buck on the internet unless you are selling a single item. A blog or website is a great place to start, followed by offering your skills, products, and services regularly.

Additionally, you can test websites, take surveys, and sell used stuff online, which take only a few minutes to set up. Alternatively, you can earn passive income by renting out your car or participating in affiliate marketing.

What are the best ways to make money at home quickly?

You can earn money from home by selling used clothes and electronics, babysitting, or renting out a room on a vacation rental site.

Is it possible to earn real money online?

There are thousands of people who are making money online right now, proving that it is possible. It’s recommended you have multiple streams of income when making money online. For example, in addition to writing a blog and having a YouTube channel, you might offer your graphic design and tutoring services as well.

When you reach that point, making money online can become a full-time occupation. Be sure to utilize budgeting tools if it does. In spite of all the advantages of self-employment, a steady cash flow is rarely one of them. As such, in order to maintain control over your finances, you must maintain a regular budget.

How can I make money at home legally?

You can earn money online in a number of legitimate ways. These include:

- Consulting or freelancing

- Providing customer service or virtual assistance from home

- Taking part in paid surveys or market research

- Making and selling handmade crafts online

- Offering physical products online through an online store or marketplace

- Selling digital products and services

- Creating your own blog or website and making money from advertising or affiliate marketing

- Create a YouTube channel

- Renting or selling items you own, such as clothing, electronics, vehicles, or guest bedrooms.

Is it possible to earn money online with no money down from home?

With no money down, it is possible to earn money online from home.

By using free or low-cost methods like online marketing, social media, and content creation, you can start a business with little or no money. Partnering with another business or selling products and services on a commission basis is also an option.

The post 20 Real Ways to Make Money From Home For Free appeared first on Due.

[ad_2]

Source link